Spare Parts Know-How

Spare parts inventory: The forgotten investment?

Inventory management is one of the most important management disciplines in every company that holds inventory. Inventory can provide the capability to meet a customer need, repair a broken machine, assemble products for sale or just keep production going.

For manufacturing organizations, direct inventory (raw materials, works in progress and finished goods) can account for up to 50 percent (or more) of the current assets of the business. Current assets are those investments that are expected to be converted to cash within the next 12 months. For retail and wholesale businesses, the figure is even higher. This type of inventory is part of what is referred to as working capital.

This working capital is tied up in the inventory, and so by definition not available for any other use until converted from an asset into cash via sales. The goal, therefore, of any business with significant working capital tied up as inventory is to convert that capital to revenue as quickly as possible. They do this by focusing attention on supply chain management, production planning and sales and operations planning.

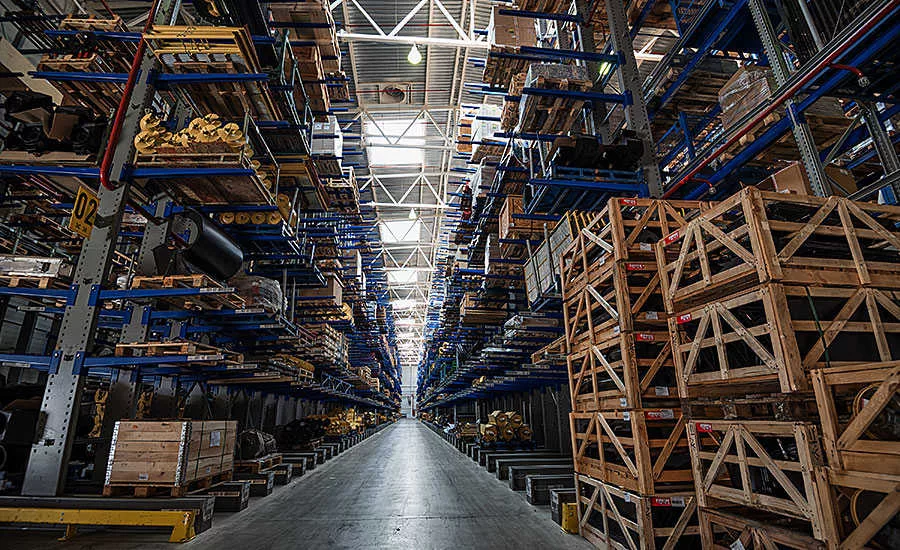

For manufacturing organizations there is, however, another element of working capital that does not get this high level of attention. This is the indirect inventory and more specifically their spare parts inventory.

This inventory is not purchased with further processing and sales in mind and so does not represent a potential future stream of revenue like direct inventory. This inventory is purchased to fulfil the functions of maintenance, repairs and operational support. (And hence is sometimes referred to as MRO inventory.) One of the major challenges that companies face in managing this indirect inventory is that if the items are not consumed during their useful life, there is no way to recover the funds invested. Selling excess and obsolete stock rarely yields more than pennies in the dollar.

It would, therefore, be natural to expect that a company spending cash on something for which there is little prospect of financial recovery would have in place very tight controls on the purchase of the items.

Yet many companies buying this type of inventory often have fewer controls over the purchase decision-making than they do for their direct inventory. Of course, there will be purchasing authorities but often the decision-making on what to stock and how many to stock is ad-hoc and emotional. Decisions are left to people with little or no training in spare parts inventory decisions, so they buy too many with their initial purchase. Then there is little, or no, end-of-life planning so companies are left with significant obsolete stocks.

This type of inventory, it seems, is considered by many senior managers to be too low level to warrant a lot of attention. This means the cash impact of investing in this type of inventory is not always fully appreciated by others in the company.

This results in the investment in spare parts inventory being often ignored until the level of cash invested in the inventory gets too big to ignore. By then, however, the money has been spent and there is little prospect of recovery.

In many ways, spare parts inventory is the forgotten investment and it is only when senior management shakes loose its apathy toward this inventory that companies can make significant inroads into reducing money wasted on unnecessary inventory. NP

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!