2024 brings new records for meat department dollars and pounds

Fresh meat increases dollar sales by 5.3% in December.

Photo credit: Fred Wilkinson

December review

- The University of Michigan Consumer Sentiment Index soared 14% in December 2024, reaching its highest rating since July. The university attributed the sharp increase to consumers believing inflation will slow further and the economy will improve in the near term. The Index rose across the population, including all ages, income levels, education and regions of the country. Sentiment is now just shy of the midpoint between the pre-pandemic reading and the historic low reached in June 2022.

- With more than two-thirds of the U.S. economy fueled by consumer spending, this rising optimism tends to translate into greater spending. This was certainly reflected during post-Thanksgiving through the end-of-year shopping patterns. The Circana survey of primary shoppers found that 54% got restaurant takeout in December and 51% dined at restaurants — among the highest shares in years. At retail, total and food and beverage dollar sales gained 2.1% in December, though unit sales were flat. The fresh perimeter increased sales by 3.5% with units up 0.4% over December last year. It is important to note that December sales reporting went through 12/31/2023 last year and 12/29/2024 this year, which may move some of the New Year’s meal dollars into the January 2025 report.

- 2024 ended up being a strong year for grocery retailers, with total food and beverage sales of $922 billion. Sales rose 3.0% in dollars and 1.3% in units. Everyday demand was strong due to purchasing restaurant food less often while cooking more in an effort to save money. Holidays and special occasions remained a time when consumers splurged a bit more prompting new records for many of the big national holidays.

Inflation insights

In December 2024 (the four weeks ending 12/29/2024), the price per unit across all foods and beverages in the Circana MULO+ universe stood at $4.35. This reflects an increase of 2.3% over December 2023. Fresh food prices averaged $4.45, which was an increase of 3.1% over December 2023. The upswing in December prices was influenced by substantial inflation in eggs, beef and other areas. Center-store prices averaged $3.93, an increase of 2.1% over December 2023. Compared to the pre-pandemic baseline, the average price per unit of $4.35 is 42.2% higher than the 2019 average of $3.13.

The average price per pound in the meat department across all cuts and kinds, both fixed and random weight, stood at $4.63 in December 2024, up 4.2% year-on-year. Processed meat prices rose the least in December, at +2.4%.

December brought a mix of price movements. The two largest proteins, beef and chicken, each increased by about 4%. Only exotic (which includes bison) experienced a decrease in prices. Over the full year, most proteins experienced mild price increases with the exception of beef that had about 5% inflation.

Meat buying dynamics in 2024

The meat department enjoys very high household penetration, with more than 98% purchasing meat at least once a year. Importantly, the meat department drove far more trips in 2024, converting on the additional total store trips. Averaging 54 trips per year, meat was purchased more than once a week — the highest number in many years.

As higher-income shoppers have moved to larger pack sizes, the units per trip are down a little, but remained around two packages, reflecting a slight increase in the spend per trip and a 5.4% increase in the spend per buyer in 2024.

Meat sales

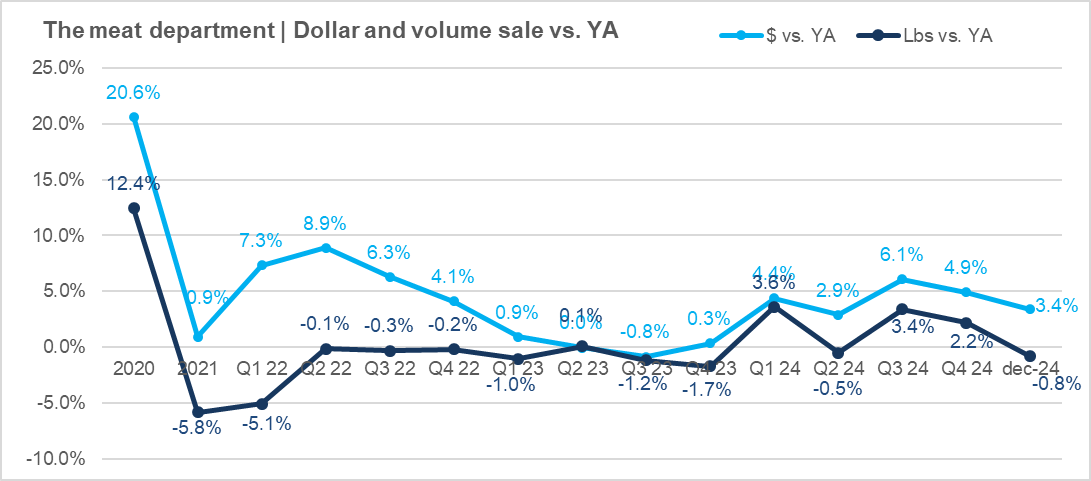

Fresh meat increased dollar sales by 5.3% in December, easily offsetting the slight 0.6% decrease in processed meat, leading to an overall 3.4% increase over December 2023. The four December weeks generated $8.9 billion, with $6.2 billion for fresh meat. While inflation played a role, pound sales increased by 0.3% in fresh, but this result was pulled down by the 2.9% decrease in processed for an overall loss of about 1% year-on-year.

It is important to keep in mind that the date cut-off in both years is likely to have impacted the December results. The months always run through a Sunday, which meant December 29 in 2024 and December 31 in 2023. The difference lies in the New Year’s celebration dollars that will likely shift to the January 2025 report, at least in part.

In calendar year 2024, dollar sales gained 5.3%. This increase reflects a combination of mild price increases and pound gains of 2.3%. Importantly, pound sales are also easily ahead of two years ago, at +1.9%.

The Wednesday holiday timing and different date cut-offs in 2023 and 2024 wreaked havoc on the week-by-week comparisons as purchases shifted by half a week. That meant sales during the first three weeks were down year-over-year, but the last week had very strong dollar and pound gains reflecting much of the Christmas spend. This also indicates that much of the New Year’s celebrations spend is likely to be reflected in the January 2025 report.

The Wednesday holiday timing and different date cut-offs in 2023 and 2024 wreaked havoc on the week-by-week comparisons as purchases shifted by half a week. That meant sales during the first three weeks were down year-over-year, but the last week had very strong dollar and pound gains reflecting much of the Christmas spend. This also indicates that much of the New Year’s celebrations spend is likely to be reflected in the January 2025 report.

Assortment

Meat department assortment, measured in the number of weekly items per store, averaged 455 SKUs in the fourth quarter, the highest of all four quarters.

Fresh meat sales by protein

While beef prices are 3.7% higher than last year, pound sales increased 4.9% in December, which was far better than the results seen in chicken and beef. Much of the growth is driven by ground beef, as seen later in this report.

The entire fresh meat aisle had a strong 2024 performance with gains for all but veal. In the full-year view, lamb had the highest year-on-year pound increases, at +12.2%, followed by beef and exotic (mostly bison).

Processed meat

Processed meat reflects a range of performances in December. While packaged lunchmeat and smoked ham decreased year-over-year in pound sales, processed chicken had a big month. The full-year performance was far better for processed meat. Both dollar and pound sales were stable, reflecting pound gains for dinner and breakfast sausage, bacon and processed chicken.

Grinds

Ground beef had another enormous month, with $1.2 billion in sales during the four December weeks. This was an increase of 9.7% in dollars and 4.4% in pounds versus December 2023. Ground lamb and chicken were other protein with double-digit increases, albeit off a smaller base. The December and 2024 results show that grinds were a clear customer favorite in an effort to balance the budget.

What’s next?

With New Year’s falling on a Wednesday in 2024, it is likely that some of the holiday’s substantial sales moved into January. New Year’s resolutions typically affect January sales patterns as well. A host of surveys found the typical themes of saving money, selfcare, eating healthier and exercising more.

- Stressing the economic advantage of home-cooked meals can be a way for grocery retailers to address consumers’ desire to save money in the new year. This includes deli-prepared meals and ingredients that provide restaurant convenience at lower prices. Deli-prepared meat grew by double digits in 2024, but is largely driven by fried and rotisserie chicken. Other proteins have an opportunity to expand sales into deli-prepared to address time-saving convenience. Retailers successfully explored ribs and meatloaf, for instance, though often on limited-time offer basis.

- Consumers are increasingly seeking balance in physical health and emotional wellbeing. On the one hand, they seek to understand more about nutrients along with their functional benefits. They appreciate on-pack callouts and healthy recipe suggestions. On the other, selfcare is fueling the everyday indulgence, whether a confectionery treat, bakery snack or a steak to celebrate the day.

- Shopping and sales patterns in the first quarter of 2025 are likely to resemble those of the latter half of 2024. Consumers remain hyper-focused on price and promotions, shopping more often and including more channels. Everyday-low-price formats have been gaining share, making promotional reach for hi-lo formats more important.

Date ranges

2023: 52 weeks ending 12/31/2023

2024: 52 weeks ending 12/29/2024

Q1 2024: 13 weeks ending 3/31/ 2024

Q2 2024: 13 weeks ending 6/30/2024

Q3 2024: 13 weeks ending 9/29/2024

Q4 2024: 13 weeks ending 12/29/2024

December 2024: 4 weeks ending 12/29/2024Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!