Fears of a dramatic shortfall in beef supply have yet to materialize

Seasonal demand is likely to underpin beef prices in May and June.

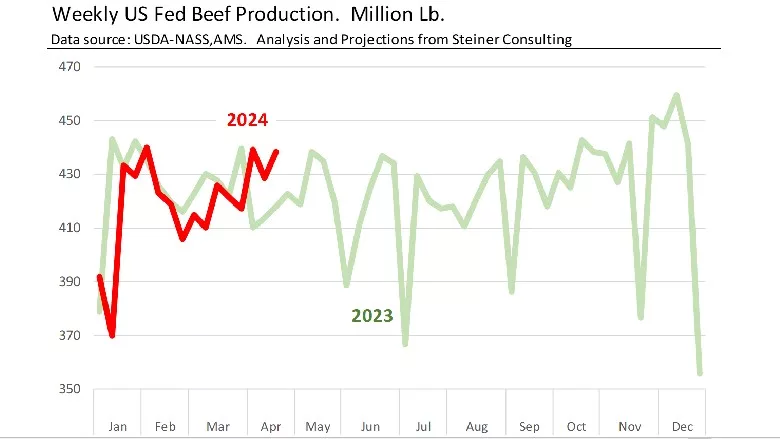

Image courtesy Steiner Consulting

Beef supply is on track to decline through 2026, but the timing and magnitude is yet to be determined.

That is because the challenge, from a supply perspective, will come when producers decide to divert a larger share of female calves to the cow herd. However, that has yet to happen. The number of heifers on feed as of April 1 was 1.1% higher than last year. More important, the share of heifers in feedlots is still well over 38% compared to 34% or less when herd rebuilding was well under way.

Drought conditions forced producers to push more calves into feedlots last fall. Combined with a slowdown in slaughter during Q1, this has resulted in more cattle on feed this spring. As of April 1, 2024, there were 1.5% more cattle on feed than the year before. The supply of long fed cattle (+120 days) was as much as 11% higher than last year.

This is good news if you are a beef buyer looking at feature opportunities for Memorial Day and Father’s Day. It is also good news if you are a restaurant operator concerned about menu price inflation this summer.

Beef prices reflect current supply conditions, and that supply is higher than it was last year. In the first three weeks of April 2024 fed beef production (i.e., beef from steers and heifers) has averaged 5% above last year. This is partly due to the increase in feedlot supplies as well as a significant increase (+3%) in carcass weights.

Wholesale beef prices, especially the price of high value cuts such as ribeye steaks or tenderloin, has been drifting counter seasonally lower. Other steak cuts, be this flank steaks, or flap meat, or even sirloin cuts, have been steady or below year-ago levels.

Seasonal demand is likely to underpin beef prices in May and June. But fears of a dramatic shortfall in beef supply have yet to materialize. It does not mean that they are not real, just that a delay in rebuilding the herd means more beef today and even less beef down the road.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!