Late Easter delivers a big April for the meat department

The average price per pound in fresh meat was also markedly lower in April 2025 compared to the full year.

Image by Nicholas Lapierre from Pixabay

April 2025 review

- The University of Michigan’s Consumer Sentiment Index showed an April reading of 52.6, which reflects a 34.2% year-over-year decline. The university attributes this to paralyzing levels of uncertainty driven by inflation, tariff talk, stock market volatility and personal finances.

- Circana research finds continued elevated levels of at-home meal occasions driven by widespread consumer concern. Circana found that 74% of consumers are somewhat or very worried that there may be an economic recession in the U.S. within the next few months. Additionally, consumer support for tariffs declined sharply from a net +10 in January to -6 in March (total support minus total opposition). Consumers report being concerned about the potential impact on prices, product availability and employment.

- In response, 66% of consumers are watching their spending on groceries and other everyday items more closely and 44% of consumers have been trying to cut back on what they consider non-essentials.

- In an effort to curb perishable food waste and capitalize on sales promotions, consumers continued to purchase groceries more often with the most recent 52 weeks showing a 4.4% increase in trips year-over-year and the latest four weeks reflecting 2.3% growth. However, the average number of units per trip continues to be flat or down for most categories. The meat department is seeing similar patterns. More than 98% purchased fresh meat/poultry at least once in the past year (unchanged), while the number of trips per buyer rose 4.8% to an average of 54.9 transactions. Additionally, shoppers spent more per buyer, at $893 over the past year, up 6.7%.

- The April numbers are heavily impacted by the shift in Easter which fell substantially later in 2025 (April 20th) than in 2024 (March 31st). This shifted holiday volume from March to April (and from the first to the second quarter), but also impacted promotional levels, prices, etc.

Inflation insights

In April 2025 (the four weeks ending 4/27/2025), the price per unit across all foods and beverages in the Circana MULO+ universe stood at $4.32. This reflects an increase of 2.5% over April 2024. This is very similar to the first quarter of 2025 average and increase. Center-store prices averaged $4.01, an increase of 1.0% over April 2024. Fresh food prices averaged $4.32, which was an increase of 4.8% year-over-year. Eggs continued to have a substantial impact on the overall fresh perimeter and total store price points. On a per unit basis, eggs averaged $7.12, which was down from $8.00 in March, but reflects an increase of 58.6% versus April 2024. Importantly, the average price per unit is also impacted by the shift in Easter. Retailers tend to run aggressive promotions in advance of major holidays, which would have affected March in 2024, but April in 2025.The merchandised share of total food and beverage dollars increased by 4.3% in April 2025 to an average of 27.3% across all foods and beverages.

Promotional investment into smoked ham, in particular, promoted deflation in processed meat. The average price per pound in fresh meat was also markedly lower in April 2025 compared to the full year. This is largely due to the shift in Easter promotions from March to April.

The average price per pound at the category level was a mix of ups and downs in comparison to April 2024. Turkey, exotic meat/poultry (which includes quail) and smoked ham invested in Easter-related promotions, pulling down the average price per pound far below last year’s everyday pricing levels. In contrast, beef, chicken and lamb experienced inflation. The April rate of increase in the average price per pound for beef accelerated in comparison to the full-year view, at +8.5% versus +4.9%.

Meat sales

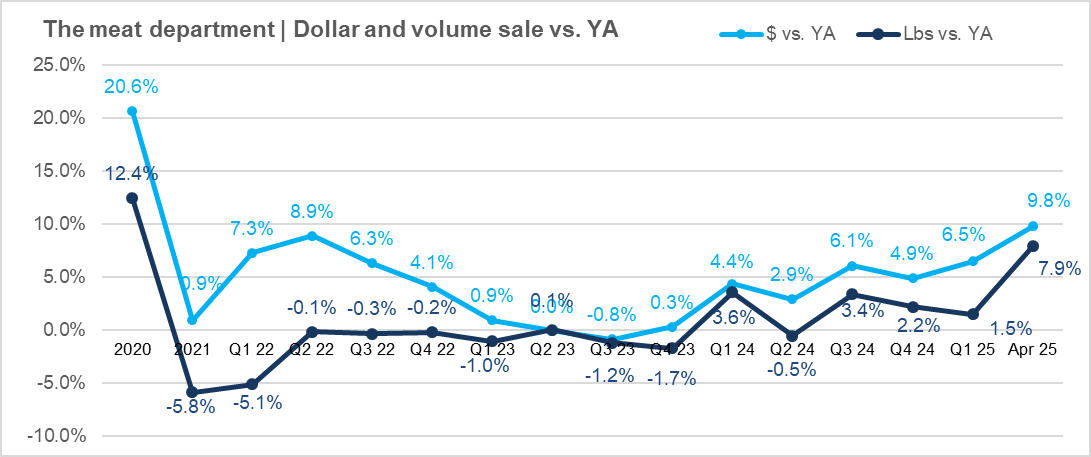

As the third-largest meat holiday behind Christmas and Thanksgiving, the three-week shift in Easter timing had a substantial impact on meat sales in April. The department grew dollar sales by 9.8% versus April 2024 and pounds increased by 7.9%. Both fresh and processed meat had strong April results.

Meat sales started gearing up the week before the holiday (the week ending April 13th). The holiday week itself was massive. Sales reached $2.27 billion, up nearly 20% in dollars and 21.6% in pounds compared to the same week in 2024. Sales levels remained elevated in the post-holiday week, with an increase of 2.1% in pound sales year-over-year.

Meat sales started gearing up the week before the holiday (the week ending April 13th). The holiday week itself was massive. Sales reached $2.27 billion, up nearly 20% in dollars and 21.6% in pounds compared to the same week in 2024. Sales levels remained elevated in the post-holiday week, with an increase of 2.1% in pound sales year-over-year.

Assortment

Retailers invested in meat department assortment for the Easter holiday, measured in the number of weekly items per store. At an average of 453 SKUs in April 2025, assortment rose 1.2% over April 2024.

Fresh meat sales by protein

Holiday classics, including turkey and lamb, showed aggressive year-over-year growth rates — keeping in mind sales are compared to everyday demand in 2024 due to the Easter date mismatch. For lamb, this means continued growth with the annual view showing 11.5% in pound growth, now closing in on being a $1 billion category. Beef impressed once more. Despite the 8.5% increase in the average price per pound across cuts, pounds grew 5.6% in April. The annual rate of increase for beef pound sales was 6.1%, which was the second-highest rate of increase behind lamb.

Processed meat

Easter powerhouse, smoked ham, had tremendous year-over-year increases in dollars and pounds in April, but a slight 1.6% volume decline in the full-year view. Bacon and sausage, especially breakfast sausage, had a strong April also.

In a late April survey, Marriner Marketing found that 32% of Americans are eating fewer eggs for breakfast — either preparing fewer per occasion or making them less often. Instead, these consumers are eating more cereal (54%), toast, bagels or other baked goods (47%), oatmeal, grits or other hot breakfast items (43%), and breakfast meats such as sausage or bacon (30%). As such, the continued high levels of egg inflation due to Avian Influenza appear to be at least one of the reasons for the strength in bacon and breakfast sausage sales in April.

Easter comparison

When comparing the floating two weeks in advance of Easter in 2024 and 2025, a picture of the true holiday performances emerges. The two core Easter weeks in 2025 generated $4.4 billion in fresh and processed meat sales compared to $4.0 billion in the two weeks leading up to Easter in 2024. Year-over-year dollar gains were highest for fresh meat. In pounds, the core Easter sales weeks in 2025 generated 944 million in pound sales compared to 896 million pounds sold during the two weeks leading up to Easter 2024. Pound gains were also highest for fresh meat.

Grinds

Though ground beef typically has a more subdued performance during key holiday months, sales continued to grow in April, at +1.1% over April 2024. Ground lamb sales, while strong all year, appear to indicate that some consumers chose ground lamb as their Easter protein. Ground chicken sales continued to be strong in April.

What’s next?

- While economic headwinds are real, the food industry is showing remarkable resilience. Holidays and celebrations remain a time when consumers are willing to spend a bit more, as illustrated by the robust spikes in Easter-related sales.

- May features Mother’s Day and the unofficial start of the grilling season in Memorial Day. Mother’s Day was traditionally one of the largest restaurant occasions, but celebrations have been more home-centric since 2020. Cross-merchandising displays facilitating planning, shopping and preparation are proven ways to drive sales, including online purchase suggestions and cross-merchandising.

- Tariff talks continue to evolve and while poorly understand by consumers are cause for concern nonetheless.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!