Strong summer demand drives meat category sales

Despite some consumers pointing to planning to eat out less often to save money during these inflationary times, 80% of consumers have ordered from or eaten at a restaurant in the past few weeks.

More than half, 54%, have ordered restaurant takeout and 49% have dined in. Restaurant engagement is far higher among households in their prime child-rearing years: Older Millennials and Gen X, shoppers ages 32 to 56. The early pandemic months saw lower consumer mobility and more time in the kitchen. As life’s hectic pace has resumed, the eternal battle between time/convenience, healthfulness and money has intensified in the past year. This has resulted in very complex consumption and shopping patterns. We see the same household take to scratch cooking one day and value-added or deli solutions the next.

We see ultra-premium and pure value items in the same basket. We see consumers switch seamlessly between quick frozen meal solutions or fresh meal kits and spending hours on cooking meat on the smoker. There is no one-size-fits-all way to handle inflationary pressures in 2022.

The July edition of the IRI monthly survey of primary shoppers underscores the market complexity.

- Awareness of grocery inflation is widespread and consumers list examples of price inflation across virtually every department in the store. Unchanged from last month, eight in 10 grocery shoppers made changes to what and where they purchased. The dominant changes are looking for sales specials (49%), skipping non-essentials (44%), finding coupons (31%) and buying more private or other low-cost brands (32%). Despite the high gas prices, 17% cherry pick specials across retailers and 15% now do some of their shopping at lower-cost retailers.

- Sales specials, while popular, are only slowly gearing up and are still far below pre-pandemic levels. Consumers are taking notice: 54% say fewer of the items they want are on sale and 44% say items are not discounted as much as they used to be.

- The share of home-prepared meals dropped to its lowest point in years, at a consumer-estimated 78.2% of all meals. The average share of home-prepared meals is higher among low-income shoppers, at 78.9%, versus high-income shoppers, at 76.1%.

- Online shopping jumped up in July to 19% of trips. Those who have integrated online shopping into their lineup are enjoying the convenience but grocery e-commerce has also emerged as a money-saving measure to help control the total basket spend. Online shopping likely also got a bit of a bump due to the latest COVID-19 variant: 26% of Americans were extremely concerned about COVID-19 in July. While less than half of the initial level of concern, it still means changed shopping and consumption patterns for one-quarter of Americans.

These measures have resulted in prolonged unit and volume pressure across most categories, while dollar sales are boosted by inflation. To document the ever-changing nature of the marketplace, IRI, 210 Analytics and Marriner Marketing continue to team up to bring the latest trends and analysis relative to meat department sales, including fresh and processed items.

Inflation insights

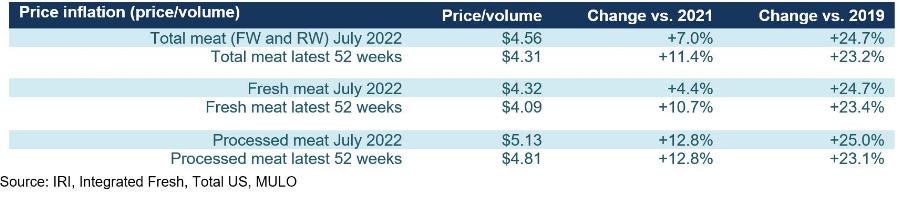

The price per unit across all foods and beverages in the IRI-measured multi-outlet stores, including supermarkets, club, mass, supercenter, drug and military, accelerated further to an increase of 13.3% in the five weeks ending July 31st, 2022 (“July”) versus year ago. This is up from +12.3% in June. July inflation was +15.3% in the center of the store (grocery) and +12.6% for perishables. Compared with July 2019, prices across all foods and beverages were up 25.2%.

The average price per pound in the meat department across all cuts and kinds, both fixed and random weight, stood at $4.56 in July 2022, which was up two cents from the June level, though up 7.0% versus year ago. This means meat had below-average inflation compared to totals food and beverages. In the past few months, meat inflation has been milder than the 52-week average, indicating that the increases are moderating. Inflation in processed meat did stay in the double digits, at +12.8% in July 2022.

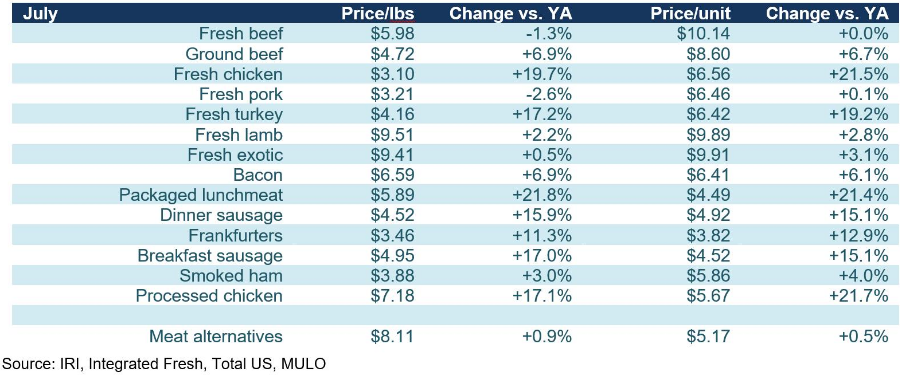

On the fresh meat side, July inflation was highest for chicken and turkey while beef prices were down. Fresh exotic prices were up a mere 0.5% in July. This includes bison that has consistently had much lower rates of inflation throughout the pandemic.

Meat sales July 2022

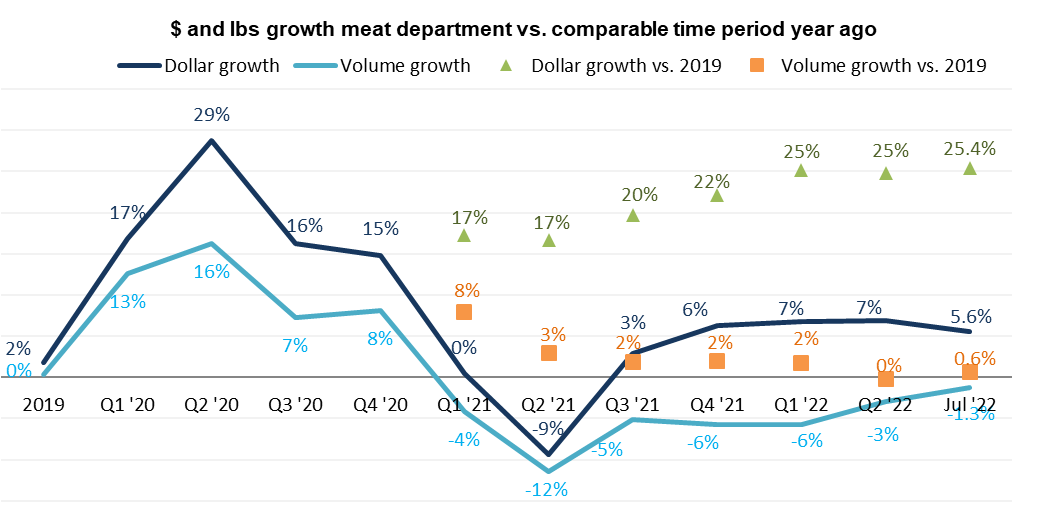

July pounds tracked slightly ahead of the volume sales seen in 2019. This meant slight year-on-year declines of -1.3%, predominantly driven by processed meat.

The strong July performance is a continuation of a sales trend line that has moved volume closer to year ago levels for a while now. The year-on-year volume declines were steepest in the second quarter of 2021 when sales went up against the incredible early pandemic peaks. Volume was a mere 1.3% behind year ago levels in July.

Assortment

Assortment

The strong July performance was especially impressive as the average assortment was down 3.5% versus year ago and 6% versus 2019. That means fewer items have to work harder to achieve the same sales results and assortment optimization becomes more important.

Fresh meat by protein

Total fresh meat sales were up 4.0% in July. Poultry delivered big, but this was inflation driven. The impact of the very inflationary levels in poultry is clear with beef and pork growing pounds year-on-year versus declines for chicken and turkey.

Processed meat

Processed meat dollars grew over the 2021 sales levels by +8.8% in July 2022 and the growth performance was supported by all areas. Packaged lunchmeat surpassed bacon in July sales with a big inflationary boost. In pounds, however, all items were down versus year ago levels, with two exceptions of processed chicken and frankfurters (hot dogs).

Grinds

July was a good month for power seller ground beef with dollar growth versus year ago, two years ago and the pre-pandemic 2019. The second-largest seller, ground turkey, also grew as did chicken. Areas that lost a little ground in comparison to last year’s sales were ground lamb and veal. While the fourth-largest seller, ground pork is winning story with a year-on-year volume increase of 16.8%. Ground pork was up 30.1% in pounds versus 2019.

What’s next?

The BLS Consumer Price Index came down some in July due to decreases in the cost of gasoline and airline tickets. This may provide consumers with some budgetary relief. However, grocery price increases continued to accelerate. As such, inflation will continue to have a profound impact on grocery and total food spending.

The July IRI survey found that:

- 45% of American households describe their financial situation as being worse than a year ago, unchanged from June.

- 43% are having some or a lot of difficultly affording needed groceries.

- 34% feel their financial situation one year from now will look worse than it does today.

The next performance report in the IRI, 210 Analytics and Marriner Marketing series will be released mid-September to cover the August sales trends.

Please thank the entire meat and poultry industry, from farm to store, for all they do.

Date ranges:

2019: 52 weeks ending 12/28/2019

2020: 52 weeks ending 12/27/2020

Q1 2021: 13 weeks ending 3/28/2021

Q2 2021: 13 weeks ending 6/27/2021

Q3 2021: 13 weeks ending 9/26/2021

Q4 2021: 13 weeks ending 12/26/2021

Q1 2022: 13 weeks ending 3/27/2022

Q2 2022: 13 weeks ending 6/26/2022

July 2022: 5 weeks ending 7/31/2022

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!