Recovery in cattle numbers does not appear imminent

Producers have indicated that they do not plan to make any significant changes to their breeding plans in 2025.

For much of 2024, we observed that US producers did not appear to be expanding the cattle herd. The share of heifers coming to market remained high by historical standards, and the expected small calf crop limited overall supply. There was some hope that producers may have bred more cattle than they initially indicated at the start of 2024, potentially setting the stage for a slow rebound in cow numbers. However, that did not happen.

Herd rebuilding — The number of heifers held back for beef cow herd replacement was 0.5% lower than a year ago, and heifers held back for dairy cow herd replacement declined by 0.9% year-over-year. Notably, within the heifers retained for beef cow replacement, the number of bred cows was surprisingly 1.7% lower than a year ago. Furthermore, producers have indicated that they do not plan to make any significant changes to their breeding plans in 2025. This suggests that US cow numbers — and consequently, the calf crop and cow slaughter — will remain constrained through 2026, possibly beyond.

Beef supply outlook — In 2024, US beef production held steady, in part due to producers continuing to send a relatively large share of heifers to slaughter while also increasing cattle weights by a remarkable 3% year-over-year. Over the past three decades, there has not been a two-year period where carcass weights increased by more than 2%. Could 2025 buck that trend? That’s certainly been the case to start the year, with fed cattle weights up 4.5% y/y in the last seven weeks. While heavier carcass weights may help moderate supply reductions, they are unlikely to prevent them indefinitely. Additionally, with the potential for fewer cattle imports from Canada and Mexico, domestic beef supply in the US is expected to contract in 2025 and 2026—especially in the lean cow meat segment.

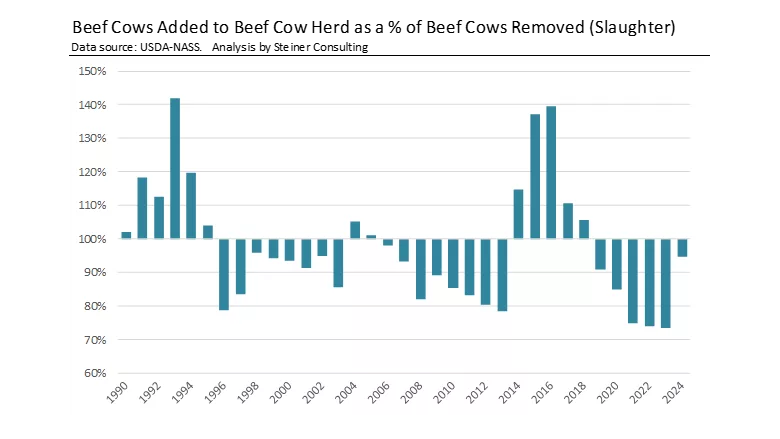

Cow meat supplies — US cow inventories declined by 0.4% compared to the previous year. While cow slaughter was down by double digits, the number of cows added to the herd was still only 95% of the cows removed. In contrast, during the herd expansion years of 2014-16, the number of cows added to the herd was as high as 140% of the number of cows removed. Given current intentions regarding replacement cow retention, a recovery in cattle numbers does not appear imminent.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!