Fewer calves in the pipeline to sustain future beef supply

Market participants along the supply chain, feedlots, packers and retailers struggle to align fixed costs with the cattle supply

The calf crop in 2025 weighed in at 32.9 million head, 1.6% lower than the previous year.

The latest Cattle on Feed report pegged the inventory at feedlots with 1,000+ head capacity at 11.5 million head, 1.8% lower than a year ago but still far from previous cyclical lows.

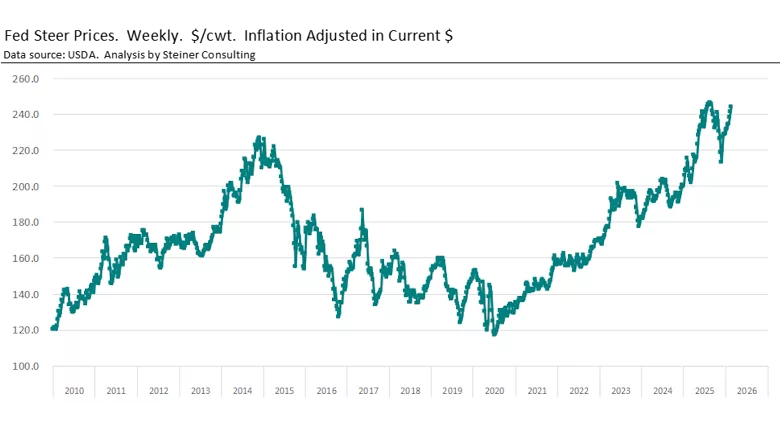

In February 2014 and 2015, the number of cattle on feed was around 10.7 million head, 7% lower than current levels. So why is it that even though the supply on feed is far from previous lows, packers are struggling to source cattle and paying near record prices for them? The chart below shows the price of fed cattle adjusted for inflation. The previous cyclical, inflation adjusted high in the cattle market was around $226/cwt. Last week, the average price was over $245/cwt, near the record prices we saw last fall.

To answer the question, it is important to take a step back and look at the entire supply chain rather than simply the supply on feed.

Much of the discussion recently has focused on excess packing capacity, illustrated by the eventual closing of the Tyson plant in Lexington, Neb., and the Tyson Amarillo plant going from two shifts to one. The combined impact of these decisions removed around 8,000 head per day of packing capacity. What has received less attention, however, is the excess capacity at the feeding level. The situation for feedlots has gone from bad to worse given that each year producers are bringing to market fewer calves than the year before. The calf crop in 2025 was 32.9 million head, 1.6% lower than the previous year. In 2024 the calf crop was down 0.4%, in 2023 it was down 2.5%, and in 2022 it was down 2%. Indeed, since 2018, the calf crop has declined every single year and by 2025 it was 3.5 million head smaller. Let that sink in for a minute. There are feedlots out there looking to buy calves to replace the ones they sell, and each year it becomes harder than the year before.

As talk of rebuilding the herd gets louder, the first step would be to divert some of the heifers currently available for feeding into the cow herd. That would further tighten feeder supplies. Last week, the CME feeder cattle index was over $377/cwt, surpassing the record price paid last fall and some 30% higher than a year ago. Indeed, since 2018, feeder cattle prices have jumped 155%. Compare this with fed cattle values, which are up 90% during this period.

For now, market participants along the supply chain, feedlots, packers and retailers, are struggling to align their fixed costs with the supply of cattle on the ground and with the level of demand in the marketplace. And that’s the real story of this cycle: not how many cattle are on feed today, but how few calves are available to sustain the system tomorrow.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!