Market Snapshot | U.S. Pork Production

China market offers potential relief to U.S. pork industry

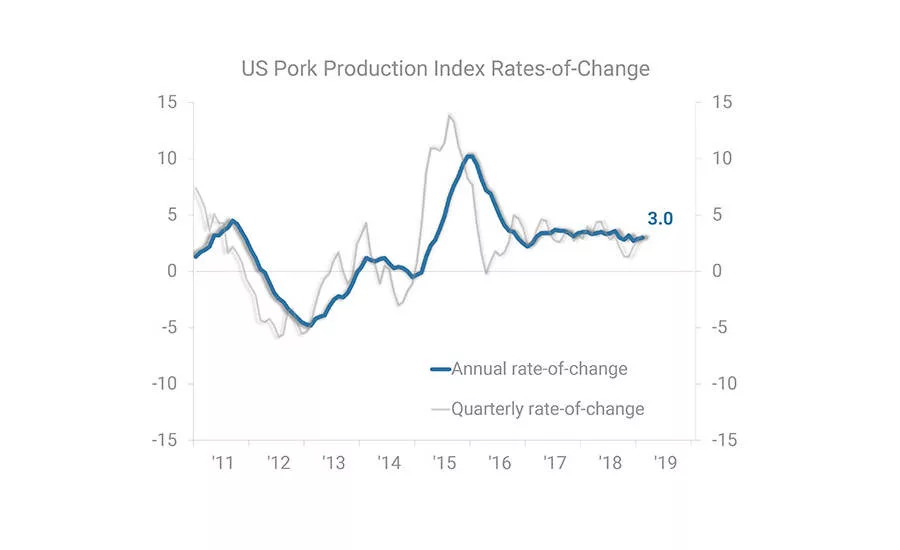

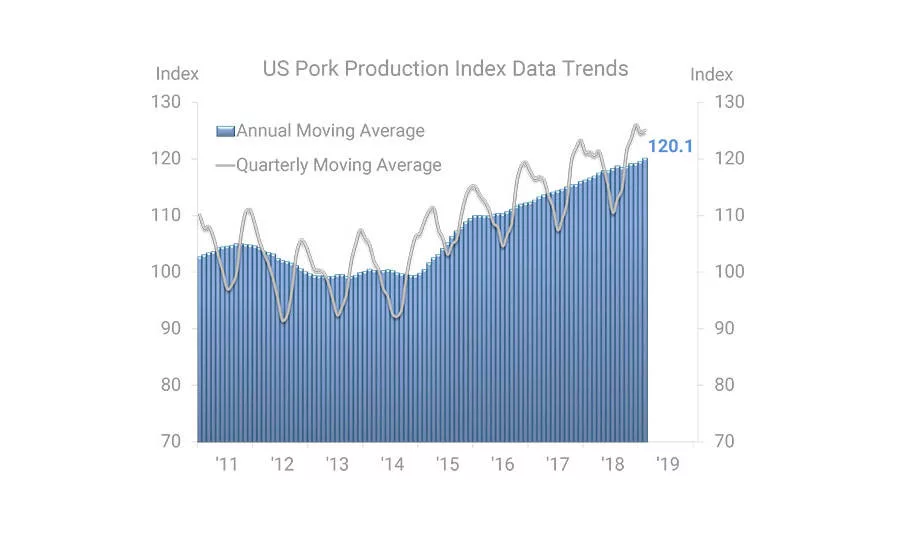

Average U.S. pork production during the 12 months through February was 3 percent higher than one year ago. U.S. personal consumption expenditures for pork moved generally lower in recent months as deflation in U.S. consumer pork prices hindered dollar-denominated expenditures. Downward business cycle momentum is evident in broad measures of U.S. consumer markets, such as U.S. total retail sales, which are in a slowing growth trend.

Despite economic headwinds rising domestically, the U.S. pork industry may see some pricing relief due to a widespread epidemic of African swine fever in China, the world’s largest pork consumer, and neighboring countries. As of late April, more than 1 million pigs had been culled to limit the spread of the disease. Most Chinese pork production is for domestic consumption; reduced herd sizes make China increasingly dependent on imports to meet demand. The U.S. is at a disadvantage relative to other pork-exporting regions due to a 62 percent pork tariff that China placed on U.S. imports last year; however, China is buying U.S. pork despite the hefty tariff. The current gap in the global supply and demand of pork is resulting in higher U.S. lean hog futures prices. NP

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!