Meat department sales shift to value-focused channels

Survey finds nearly three in 10 shoppers include more value-focused retailers into their store rotation.

Photo credit: Fred Wilkinson

Inflation continued to take the headlines in most of 2023, with consumer’ concern driven by the cumulative impact of several years of rising prices in many areas of life. This has 55% of shoppers looking for sales and deals more often, according to the year-end Circana survey among primary grocery shoppers. Other frequently applied measures include cutting back on non-essentials, exploring store brands, clipping coupons and a number of store-related moves.

The survey found that nearly three in 10 shoppers include more value-focused retailers into their store rotation, 18% shop more grocery stores to get the best deals and another 18% have switched stores altogether. This has led to substantial channel shifting when comparing the share of meat department dollars in 2023 versus the channel share distribution in 2019. According to Circana, supermarkets have lost 3 percentage points over the past three years. The shift resulted in gains for many other channels, including club, mass/supercenter and online.

Consumers estimated that about eight in 10 meals (79.7%) were prepared at home in December. This was up a few percentage points from November and typical for this time of the year. Following the holiday months, 29% plan to eat out at restaurants less often. As inflation is slowing, consumers are becoming slightly more optimistic.

- The December survey found that 58% of consumers perceive grocery prices to be “much higher,” down 4 points versus November and down 16 points from last December.

- 19% of consumers reported that their financial situation is better than last year versus 13% in December 2022.

- Shoppers’ financial outlook has also shown some improvement since 2022. While the number expecting their financial situation to be better a year from now has been steady, there are fewer who expect it to be worse, at 24% versus 31% in December 2022.

- This slowly rising optimism is likely to prompt consumers to continue to shift their dollars across items, brands, sizes, stores and restaurants. Circana and 210 Analytics will continue to track the trends in the meat department throughout 2024. The report is made possible by Hillphoenix.

Inflation insights

The price per unit across all foods and beverages in the Circana-measured multi-outlet stores, including supermarkets, club, mass, supercenter, drug and military, increased by 1.7% in December 2023 (the five weeks ending 12/31/2023) versus December 2022. The fourth quarter inflation averaged 2.1% and the total year saw the average price per unit increase by 6.1%.

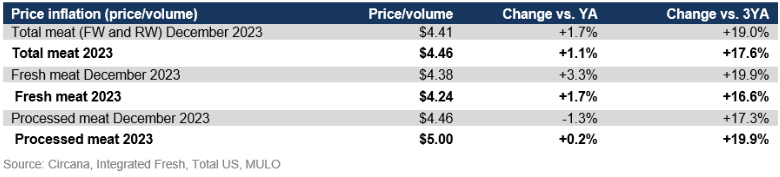

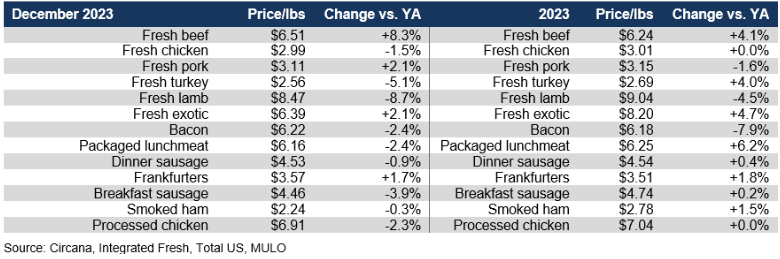

The average price per pound in the meat department across all cuts and kinds, both fixed and random weight, stood at $4.41 in December 2023, which was up 1.7% from the levels seen in December 2022. Processed meat tends to have the higher prices, but its average price per pound decreased for bacon, packaged lunchmeat, dinner and breakfast sausage and processed chicken. In all of 2023, meat department inflation was very mild, with prices up just 1.1%.

December brought year-on-year deflation for the vast majority of fresh and processed categories. Reflecting a tight market, beef prices are increasing once more.

Meat sales

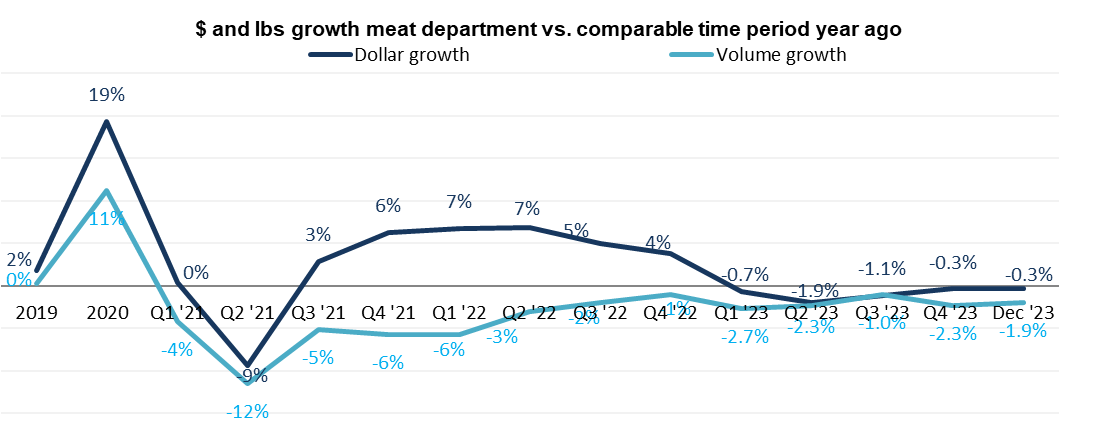

In December, pounds declined by about 2%, right in line with the rest of the year. Given the mild inflationary levels, this meant a slight drop in dollar sales overall, despite an increase for fresh meat.

The why behind the declines in the meat department sales are illustrated by Circana’s household panel metrics. Shoppers buy meat less often but these fewer trips have not resulted in bigger purchases.

The two December holiday weekends illustrate once more that celebrations are a time when consumers open up their wallets a bit further. Pound sales increased by 3.4% the week before Christmas and 2.7% the final week of the year. This underscores the importance of merchandising against all primary, secondary and self-invented holidays throughout the year.

All throughout the year volume has hovered between one and two percent behind year ago levels, whereas dollar sales has been right around year-ago levels.

Assortment

Meat department assortment, measured in the number of weekly items per store, was virtually flat in 2023 – now reflecting a fairly constant average of around 400, which is down about 25 items from pre-pandemic levels.

Fresh meat sales by protein

December had a number of welcomed increased in volume sales during a strong holiday performance. Beef and pork were the notable exceptions. In the total calendar year, chicken sales impressed with pound growth of 1.1%.

Consumers continued to purchase turkeys all throughout December with four out of the five weeks showing positive pound growth. The final week of December was especially strong with pound growth of 23.6% and corresponding dollar gains of 12.4%

Whole bird turkey sales were up compared to year ago levels by 1.3% in dollars and 14.3% in pounds. All other areas of turkey performed well also on a favorable price per pound, with the one exception of turkey legs.

Smoked ham sales were not as strong with the one exception of the final week of the year. The week ending December 31st saw a 32.3% increase in pounds and 29.2% in dollars.

Processed meat

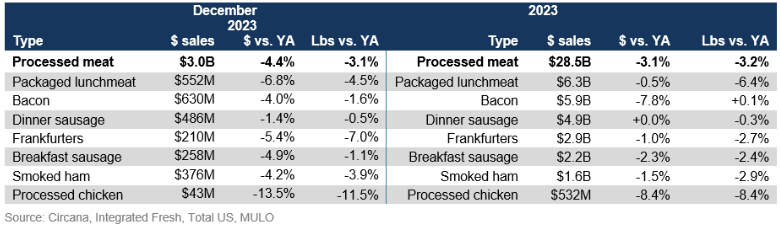

December processed meat sales were half that of fresh meat, at $3.0 billion. Dollar sales were down by 4.4% versus December 2022, while pounds decreased 3.1%. In all of 2023, dollar sales gains dropped 3.1% behind year ago levels, mostly driven by deflation in bacon and a drop in pound sales for processed chicken.

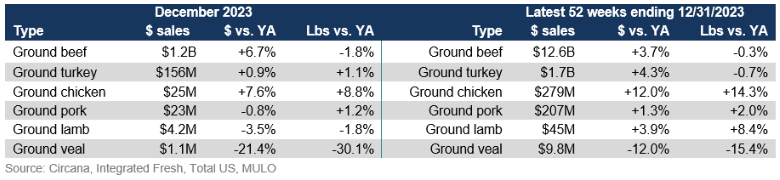

Grinds

While ground beef pounds decreased 1.8% in December, it outperformed whole muscle beef. Smaller grinds, including turkey, pork and chicken, gained in both pounds and dollars in December.

What’s to come in 2024?

Holidays remain a time when shoppers are splurging a bit more on groceries, but overall, unit and pound sales have remained subdued in the past few months despite prices starting to level off. The market typically experiences a delay in consumer demand ticking back up once prices come down. Given the duration, scope and depth of inflation that delay may be longer than normal.

The next performance report in the Circana, 210 Analytics and Hillphoenix series will be released mid-February 2024 to cover the January sales trends. To learn more about Circana’s meat and poultry sales and shopper measurements, please contact: FreshFoods@circana.com. Please thank the entire meat and poultry industry, from farm to store, for all they do.

Date ranges:

2023: 52 weeks ending 12/31/2023

Q2 2023: 13 weeks ending 7/2/2023

Q3 2023: 13 weeks ending 10/1/2023

Q4 2023: 13 weeks ending 12/31/2023

December 2023: 5 weeks ending 12/31/2023

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!