As cattle markets consolidate, importance of risk management rises

Paper profits create excitement but also fear when the market starts to turn.

It was only a couple of weeks ago that feeder cattle futures climbed past $380/cwt, a record. Just as important, the price spread between spot prices and 2026 futures narrowed considerably. The market was telling producers that current record prices were likely to persist. But despite all the bullish enthusiasm, there was always a sense of unease. There was too much speculative interest that could reverse course at the speed of a tweet.

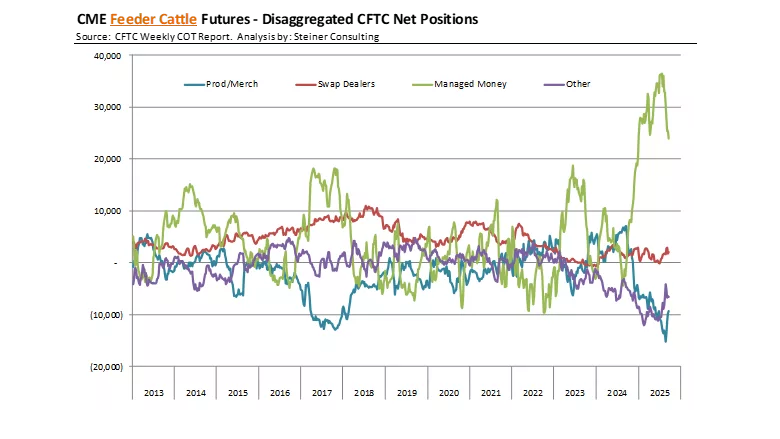

Through the summer, managed money held a net-long position of around 36,000 contracts. While they pared back some of those positions in September, their long position was still far higher than at any point in the last 15 years. As we have seen with other commodities (hogs, corn, beans, etc.), a sudden rush to reduce risk can result in wild price swings in futures. But speculative money is only one side of the coin. Producers are making the most money they ever have and also have the most money at risk for the next calf crop.

Estimates from the Livestock Market Information Center peg cow-calf returns for individual, unhedged producers at a little over $900 per cow. Even when adjusted for inflation, these are the highest returns producers have enjoyed in over 40 years, possibly ever. Based on futures earlier in the month, returns for 2026 were pegged at $825 per cow, and for 2027 were projected at $746 per cow. These paper profits create excitement but also fear when the market starts to turn. Producers could use risk-management tools to protect these margins, but invariably that means more selling activity, which again creates problems when there is so much uncertainty about future government policy.

Since that record $380 print in mid-October, nearby feeder cattle futures have declined by nearly $35/cwt (-9%). Talk of opening the door to more Argentine beef certainly had an effect, further compounded by President Trump saying producers “have to get their prices down, because the consumer is a very big factor in my thinking.” Those trading futures don’t care that producers have little say on prices in a free market. What mattered to those trading futures was that the administration was signaling a shift, favoring policies likely to pressure cattle and beef prices. More imports from Argentina would be part of this, as would a potential trade deal with Brazil, lowering tariffs on the biggest beef exporter on the planet. And to cap it off, talk of a deal with Mexico to reopen the border added further downward pressure.

The fundamentals in the US beef and cattle market have not changed. The cattle herd remains the smallest in decades, domestic beef production is expected to decline further as producers rebuild, and beef demand is having its moment. But in the short term, markets are consolidating after those frothy early-fall days. And they are offering a stark reminder that risk management should be a consistent approach, not an à la carte menu.

Steiner Consulting

Steiner ConsultingLooking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!