Meat once more rules fresh perimeter sales in November

November sales are dominated by the all-important Thanksgiving holiday — one of the largest retail opportunities in meat and many other retail departments. This makes it a hard-to-beat sales occasion any year. However, throughout October and November, shoppers’ concern over COVID-19 rose along with the number of new cases. This resulted in very different Thanksgiving celebrations versus typical years, with less travel, smaller gatherings and earlier shopping to avoid crowds. Much like seen throughout the year, elevated concern also translated into a greater spending at retail versus foodservice. During the month of November, sales for all food-related items (total edibles) increased 9.3%, which was up from 8.6% during the month of October.

The November sales build was different this year, with COVID-19 prompting earlier Thanksgiving shopping. Additionally, many people shopped earlier or diverted purchases online — in some cases encouraged by retailers to manage traffic flow during one of the busiest shopping weeks of the year. Some retailers provided free delivery, ramped up their curbside order slots and encouraged earlier shopping. Many closed their doors altogether on Thanksgiving Day to provide the team a much needed break and a few closed their doors on Black Friday, a traditionally slow day for grocery retailing. The total meat department experienced a 5.4% boost in sales the week of Thanksgiving but the two weeks leading up to the holiday week were massive for the fresh meat department, at +17.5% and +19.9%. A sign of earlier meal planning, turkey sales peaked the week ending 11/15/20 this year.

|

Meat department |

Dollar sales |

Dollar gains |

Absolute dollar gains |

|

Week ending 11/8 |

$1.53B |

+11.9% |

+$162.3M |

|

Week ending 11/15 |

$1.62B |

+17.5% |

+$241.3M |

|

Week ending 11/22 |

$1.86B |

+19.9% |

+$309.3M |

|

Week ending 11/29 |

$1.46B |

+5.4% |

+$74.8M |

|

Four rolling weeks leading up to Thanksgiving |

$6.47B |

+13.9% |

+$787.7M |

Source: IRI, Integrated Fresh, Total US, MULO

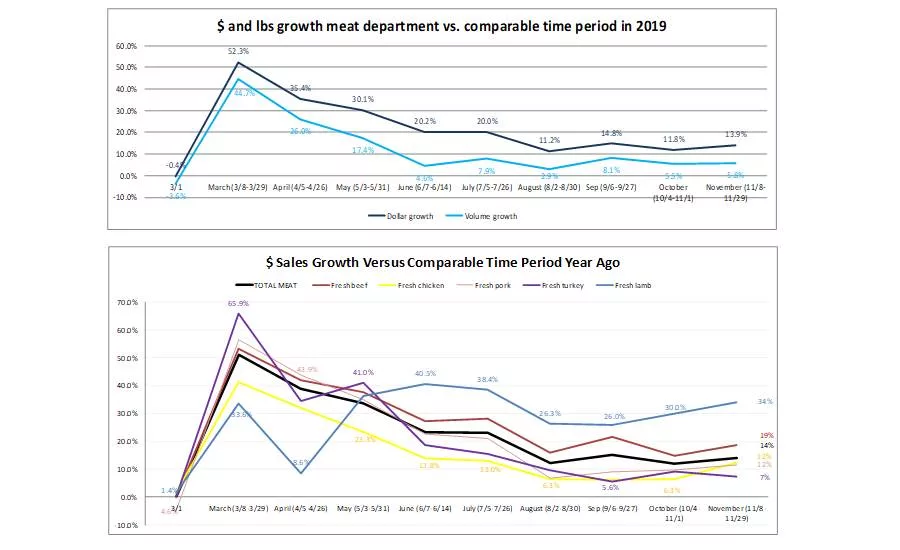

Meat department sales during the week ending November 8th through November 29 increased 13.9% in dollars and 5.8% in volume versus year ago. This reflects an increase for both dollars and volume over October.

Year-to-date through November 29th, overall meat dollar sales have increased 18.8% and volume sales have increased 10.4% versus the same period last year. This translates into an additional $12.0 billion in meat department sales during the pandemic, which includes an additional $5.3 billion for beef, $1.5 billion for chicken and $1.1 billion for pork than during the same period in 2019.

Dollar versus Volume Gains

Fresh meat had slightly higher gains in both dollars and volume during the month of November on a larger base. The gap between dollar gains and volume gains increased from 6.3 percentage points in October to 8.1 points in November.

|

% sales change (November 11/8-11/29) versus year ago |

Dollar gains |

Volume gains |

Volume/dollar gap |

|

Total meat |

+13.9% |

+5.8% |

-8.1 |

|

Total fresh |

+14.5% |

+5.2% |

-9.3 |

|

Total processed |

+12.6% |

+7.5% |

-5.1 |

Source: IRI, Integrated Fresh, Total US, MULO, % gain versus YA

Price per Volume

According to the IRI insights on the price per pound volume, beef and chicken experienced slight increases in the price per pound, whereas the prices for pork, turkey and lamb moderated a bit in favor of the consumer. The average price per volume for turkey was much lower with November being a heavily promoted month. The same is true for meat overall.

|

|

Average price per volume |

||||||||

|

|

Mar |

Apr |

May |

Jun |

Jul |

Aug |

Sep |

Oct |

Nov (11/8-11/29) |

|

Total meat |

$3.81 |

$3.75 |

$4.02 |

$4.22 |

$4.06 |

$3.96 |

$3.87 |

$3.85 |

$3.09 |

|

Total fresh meat |

$3.65 |

$3.71 |

$3.93 |

$4.14 |

$3.92 |

$3.77 |

$3.67 |

$3.64 |

$2.78 |

|

Total processed meat |

$4.19 |

$3.83 |

$4.24 |

$4.41 |

$4.39 |

$4.40 |

$4.35 |

$4.37 |

$3.95 |

|

Fresh beef |

$5.02 |

$5.32 |

$5.86 |

$6.42 |

$5.68 |

$5.42 |

$5.17 |

$5.14 |

$5.19 |

|

Fresh chicken |

$2.43 |

$2.44 |

$2.44 |

$2.48 |

$2.50 |

$2.46 |

$2.41 |

$2.42 |

$2.44 |

|

Fresh pork |

$2.87 |

$2.89 |

$3.04 |

$3.14 |

$2.90 |

$2.78 |

$2.73 |

$2.74 |

$2.73 |

|

Fresh turkey |

$3.15 |

$3.03 |

$3.37 |

$3.41 |

$3.44 |

$3.43 |

$3.43 |

$3.18 |

$1.24 |

|

Fresh lamb |

$8.28 |

$7.98 |

$8.35 |

$8.49 |

$8.52 |

$8.54 |

$8.48 |

$8.51 |

$8.38 |

Source: IRI, Integrated Fresh, Total US, MULO, % gain versus YA

During September 2020, 35.5% of all meat volume was sold on some type of promotion, whether a circular feature, display, temporary price reduction or any combination thereof. This percentage increased to 36.2% in November 2020, which was about two percentage points lower than in 2019. Processed meat is selling less meat on promotion than fresh meat. In November 2020, 33.4% of all processed meat volume was sold on promotion versus 37.3% for fresh. For smoked ham, more than half of all volume in November 2020 was sold on merchandising. In contrast, this was nearly 71% in December of 2019, so we may see continued elevated levels in the next few weeks. Fresh turkey was very aggressive in promotions this year. More than half of all turkey pounds were sold on merchandising, at 51.4%. This explains the drop to $1.24 per pound from its typical levels around $3.20 to $3.40 per pound.

Assortment

Assortment has nearly completed its comeback after dropping by more than 65 items during some of the tightest supply weeks in May and June. During the month of November, retailers typically increase the number of items to accommodate for Thanksgiving choices. While the average number of items per store increased to 544, assortment remained down 5.7% versus year ago levels although not all new item codes may be tallied just yet.

|

|

Average items per store selling for week ending… |

|||||||

|

March (3/1-3/29) |

April (4/5-4/26) |

May (5/3-5/31) |

June (6/7-6/28) |

July (7/5-7/26) |

August (8/2-8/30) |

September (9/6-27) |

October (10/4-11/1) |

November (11/8-11/29) |

|

560.2 |

532.1 |

512.4 |

508.2 |

518.4 |

523.2 |

527.0 |

529.0 |

544.4 |

|

-1.1% |

-6.4% |

-10.0% |

-10.7% |

-8.4% |

-6.7% |

-5.8% |

-5.7% |

-5.7% |

Source: IRI, Integrated Fresh, Total US, MULO, average items per store selling

Meat Gains by Protein

Lamb continued to have the highest percentage gains on its small base, at +34.0% versus the same month year ago. Lamb has seen a steady increase in its gains month-over-month. With restaurants in many states closing back down in terms of on-premise dining, it is likely that more lamb sales will continue to flow through retail. Beef’s performance continued to be astounding, up 18.7% during October. Various high-end cuts had strong Thanksgiving sales, perhaps a reflection of a choice other than turkey amid smaller gatherings. Chicken saw the smallest gains during the months of May through October, but had a strong November, perhaps with some shoppers opting for a whole bird chicken as their main meat, that increased 7.3% during November.

Processed meats had a very strong month as well. Hot dogs led percentage growth at +19.9%, but bacon and packaged lunch meat were the biggest in terms of sales.

|

|

2020 $ sales gains versus comparable 2019 period |

|||||||||||

|

|

w.e. 3/1 |

Mar |

Apr |

May |

Jun |

Jul |

Aug |

Sep |

Oct |

Nov (11/8-11/29) |

||

|

TOTAL meat |

-0.4% |

+52.3% |

+35.4% |

+30.1% |

+20.2% |

+20.0% |

+11.2% |

+14.8% |

+11.8% |

+13.9% |

$6.5B |

|

|

Processed meat |

-1.8% |

+55.0% |

+29.1% |

+23.0% |

+14.4% |

+14.1% |

+9.2% |

+13.9% |

+11.5% |

+12.6% |

$2.2B |

|

|

Bacon |

-6.4% |

+53.3% |

+47.4% |

+33.8% |

+17.9% |

+19.2% |

+14.5% |

+18.8% |

+18.2% |

+18.9% |

$496M |

|

|

Packaged lunchmeat |

-4.3% |

+47.7% |

+19.9% |

+9.4% |

+5.6% |

+5.1% |

+2.6% |

+5.9% |

+6.9% |

+9.0% |

$392M |

|

|

Dinner sausage |

2.7% |

+66.5% |

+41.3% |

+33.6% |

+20.4% |

+16.4% |

+11.2% |

+18.3% |

+12.4% |

+13.9% |

$313M |

|

|

Smoked ham |

-5.3% |

+121.8% |

+20.1% |

+67.3% |

+32.1% |

+25.9% |

+14.4% |

+9.9% |

+4.2% |

+4.5% |

$307M |

|

|

Breakfast sausage |

-4.4% |

+55.8% |

+43.3% |

+40.0% |

+22.9% |

+19.5% |

+18.0% |

+22.7% |

+15.0% |

+12.0% |

$179M |

|

|

Frankfurters |

-0.1% |

+75.8% |

+39.1% |

+20.2% |

+12.6% |

+14.2% |

+9.5% |

+26.1% |

+16.2% |

+19.9% |

$161M |

|

|

Processed chicken |

5.1% |

+40.2% |

+12.9% |

+14.1% |

+11.6% |

+6.9% |

+4.4% |

+6.8% |

+7.1% |

+16.8% |

$42M |

|

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. YA

Grinds

During November, the dominance of grinds in meat sales continued. Ground beef sales totaled $792 million or 199 million pounds. Ground beef alone added $75.6 million versus year ago levels in November. Altogether, the five grinds listed below generated an additional $90.2 million during the November weeks.

|

% sales change (November 11/8-11/29) versus year ago |

Dollar sales |

Dollar gains |

|

Ground beef |

$791.6M |

+10.6% |

|

Ground turkey |

$105.1M |

+10.5% |

|

Ground chicken |

$15.5M |

+18.8% |

|

Ground pork |

$13.6M |

+5.2% |

|

Ground plant-based meat alternatives |

$4.3M |

+23.8% |

|

Ground lamb |

$3.1M |

+28.1% |

|

Ground veal |

$0.9M |

+3.8% |

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. YA

What’s Next?

Everyday demand continues to hold around 15% above year ago levels with renewed shelter-in-place restrictions and rising COVID-19 cases likely to push more dollars to food retail once more. Additionally, the comeback of restaurants transactions is hampered by colder temperatures in northern states. Aided by the effect of online sales, trip reduction, virtual schooling and working-from-home, meat sales are likely to remain well above year-ago levels for many weeks to come.

The end-of year holiday demand is likely going to be very different, much like Thanksgiving. According to the latest weekly shopper survey wave by IRI, conducted mid-November, the holidays will involve much less travel and smaller gatherings.

- Only one in four shoppers plan to celebrate with others outside their household, about half the rate of 2019.

- One in three expect to spend less on groceries for the December holidays this year, primarily due to hosting fewer/no guests this year or cutting back to save money.

· For New Year’s, 30% plan to celebrate at home without guests, while only 5% of primary grocery shoppers plan to go to a party/gathering, 4% host others, and 3% go to a bar/restaurant. 10% celebrated last year but won’t do anything either at home or away from home to ring in the New Year (51% typically don’t celebrate).

These predictions point to many potential changes for the meat department. Much like the pandemic-affected holidays to date, packer/processors and retailers may consider messaging and promotions that help shoppers find new ways to make the holidays special at home or on a tighter budget, and retailers should plan for an earlier spike in holiday item purchasing than last year.

COVID-19 Vaccine

Despite the positive vaccine efficacy news in early November, interest in getting the COVID-19 vaccine remained stable versus September with about half planning to get it: 24% say they won’t get the COVID vaccine once it is available to them, and 28% are unsure. In comparison, flu vaccine participation is virtually flat over year ago levels as well: 51% had gotten the Flu vaccine by mid-November and another 12% still planned to get it, which would result in only a slight increase over the 58% who were vaccinated last year. The promising COVID vaccine news did not improve Americans’ personal economic outlook, with only 23% expecting their financial situation to be better next year (down from 32% in July) and 26% expecting to be worse off (18% in July).

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!