Late Easter disrupts comp sales for meat holiday classics

Average price per pound in the meat department hits $4.84 in March 2025.

Photo credit: Fred WIlkinson

In March 2025 (the four weeks ending 3/30/2025), the price per unit across all foods and beverages in the Circana MULO+ universe stood at $4.32. This reflects an increase of 3.3% over March 2024. This is very similar to the first quarter of 2025 average and increase. Importantly, the average price per unit is impacted by the shift in Easter. Retailers tend to run aggressive holiday promotions in advance of major holidays. The Easter shift resulted in a 6.3% decrease in merchandised dollars in March 2025 versus March 2024. Center-store prices averaged $4.05, an increase of 3.5% over March 2024. Fresh food prices averaged $4.31, which was an increase of 3.8% over March 2024. Eggs continued to have a substantial impact on the overall fresh perimeter and total store price points. On a per unit basis, eggs averaged $8.00, which reflects an increase of 72.2% over March 2024.

The average price per pound in the meat department across all cuts and kinds, both fixed and random weight, stood at $4.84 in March 2025, up 6.8% year-on-year. Fresh meat prices rose +4.4% in March in sharp contrast to the prices of processed meat that increased 14.0%. This is largely due to the shift in Easter timing and the delayed start to ham promotions.

Price movements at the protein level ranged from deflation for fresh exotic (mostly bison) to 65% inflation for smoked ham due to Easter promotions shifting into April. Beef prices increased a little more than 6%, whereas chicken and pork prices increased about 2%. On the processed meat side, lunchmeat prices are stabilizing, but sausage is experiencing price increases of about 5%.

Meat sales

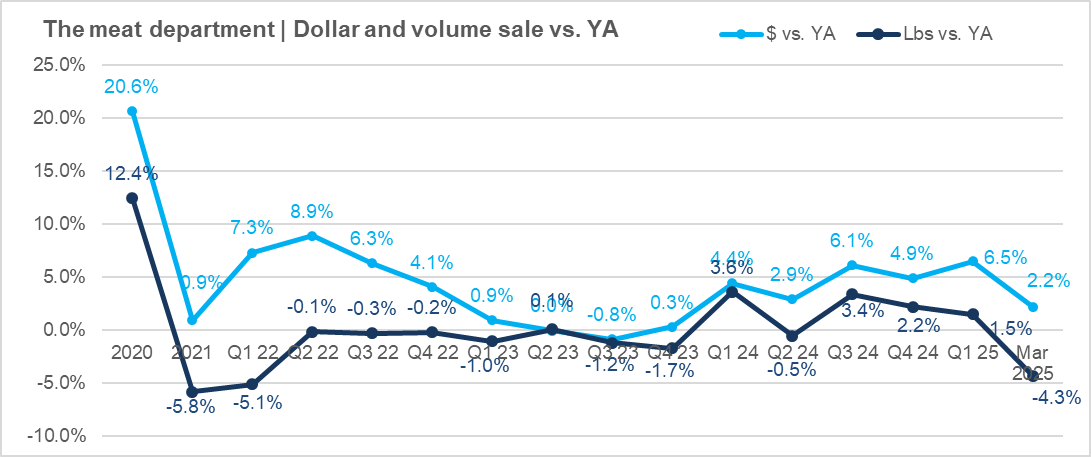

As the third-largest meat holiday behind Christmas and Thanksgiving, the three-week shift in Easter timing had a substantial impact on meat sales. While dollar sales continued to grow due to inflation, pounds dropped 4.3% behind last year’s levels. This was driven by processed meat, specifically smoked ham. Fresh meat grew dollar sales 7.5% over March 2024 levels, with a 2.9% increase in pounds. Processed meat sales declined by more than 9% year-on-year. First-quarter sales increased 1.5% in pounds and 6.5% in dollars over the first three months of 2024.

The first two weeks of March reflect everyday shopping patterns with solid dollar and pound gains compared to the same weeks in 2024. Come the third week, when holiday shopping typically starts to gear up, pounds dropped into the negative. Going up against the 2024 Easter week resulted in a 16.2% decline in pounds and 7.7% decrease in dollar sales.

Assortment

Meat department assortment, measured in the number of weekly items per store, averaged 449 SKUs in March 2025, down 1% over March 2024.

Fresh smeat Sales by protein

Beef demand continues to be strong. At +4.3%, the increase in beef pound sales matched that of chicken. Ground beef played a big role in that, but premium areas such as Ribeye and sirloin also grew pound sales year-on-year. Easter-classic lamb experienced a decrease in dollar and pound sales due to the holiday shift.

Processed meat

In addition to the Easter-related dip in smoked ham sales, all but dinner sausage lost ground in pound sales in March 2025. The pound declines were steepest for bacon and frankfurters. Given the Easter impact, the 52-week view provides a truer look at the performance of each of the processed proteins.

Grinds

Ground beef had another enormous month, with $1.3 billion in sales during the four March weeks. This was an increase of 15.2% in dollars and 6.8% in pounds versus March 2024. Ground chicken and lamb also had double-digit gains this month. During the latest 52 weeks, ground beef sales reached $15.9 billion, with a 4.9% increase in pounds.

What's next?

- For the March report, it is important to look beyond the date shift impact and focus on the longer-term trends. While March was negatively affected by the later timing of Easter, April sales will be boosted by the additional Easter volume, affecting many categories across the meat department.

- The ongoing news about tariffs has already resulted in 30% of shoppers stockpiling some items out of concerns for rising prices or out-of-stocks. This includes pantry staples such as pasta, rice and cereal (62%), canned foods (55%), bottled/canned beverages (47%), coffee (35%) and items such as home care and cleaning products.

- While the meal landscape remains home-centric, 78% of consumers did consume at least one restaurant meal in March 2025. Delivery and takeout make up an ever-growing share of restaurant sales. Gen Z and Millennials are the driving forces behind delivery and takeout. For instance, while 58% of Gen Z have gotten restaurant takeout in the past month, only 34% of Boomers have done so. Likewise, 35% of Gen Z have gotten delivery versus just 9% of Boomers.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!