Market Snapshot | U.S. Poultry

U.S. poultry market: Slow, slight slide

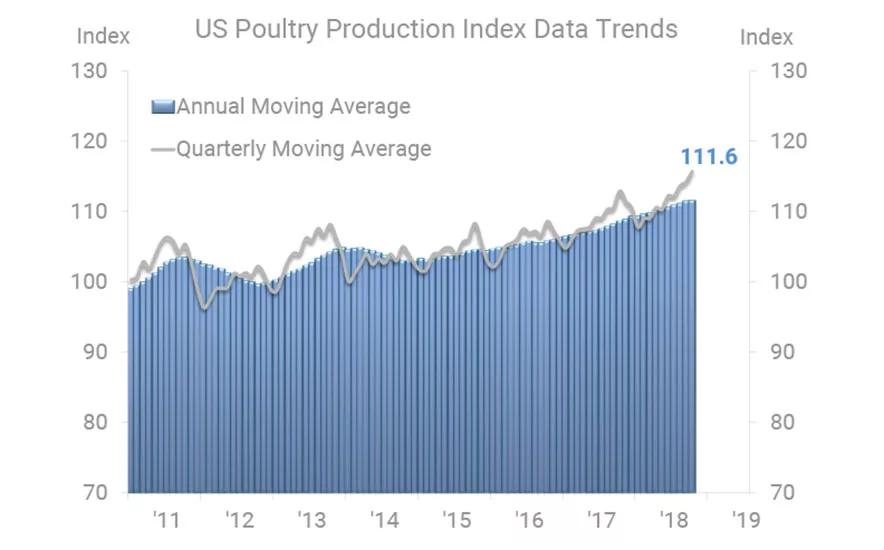

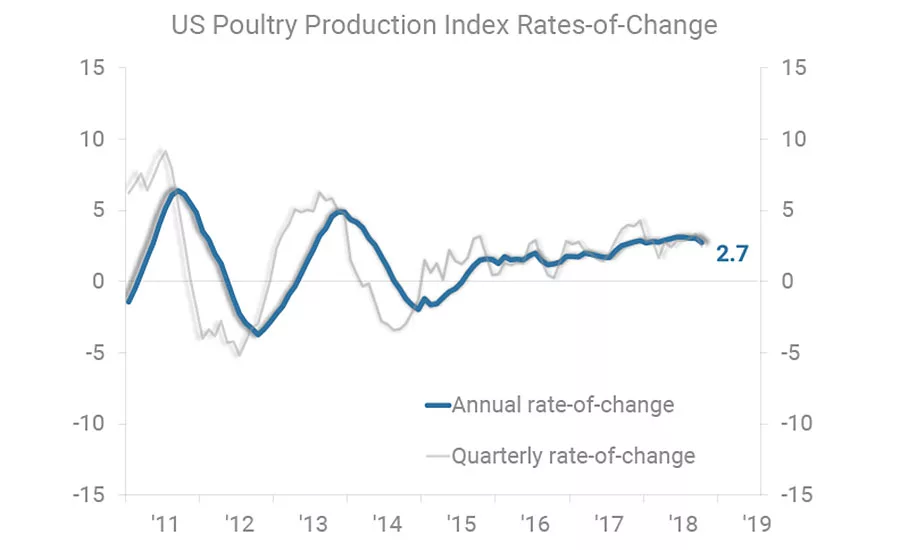

Average U.S. poultry production during the 12 months through October (latest data available) was up 2.7 percent from the prior year. The pace of growth in annual production has been slowing since June. Trends in the price of Tyson Foods stock suggest business-cycle decline (slowing growth or recession) in production will likely persist in coming months, in line with our expectations for overall U.S. food production.

Expectations for slowing growth are not limited to domestic markets. The majority of developed economies are expected to experience business-cycle decline this year, which could hinder exports. Annual U.S. chicken exports to the world peaked in April 2018 and have since declined. Exports have not recovered from a steep decline in 2015, when China closed its doors to U.S. chicken because of an outbreak of avian influenza. Annual exports in November were 27.8 percent below the record level and 2.6 percent below the April 2018 level.

Rising employment and transportation costs are additional headwinds facing the meat industry. The average U.S. Truck Transportation of Freight Producer Price Index in 2018 was 6.6 percent higher than the 2017 average. This rise was likely because of a shortage of truck drivers and an associated 4 percent year-over-year increase in U.S. average hourly earnings of truck transportation workers, a full percentage point higher than the increase in hourly earnings for the private workforce as a whole. Higher diesel prices also contributed to the rising cost of transportation. Chicken producers may see some pricing relief in 2019, as U.S. oil prices are expected to remain relatively low in the near term; however, the labor market is expected to remain tight. Companies should focus on employee training and retention efforts in order to save on the cost of onboarding new employees. NP

Editor’s Note: This is a quarterly economic update provided by ITR Economics, published exclusively in The National Provisioner.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!