July 4th, a big meat holiday, was even bigger amid pandemic

So far, the 2020 pandemic-affected holidays have seen strong sales performances. Without exception, Easter, Mother’s Day, Father’s Day and Memorial Day boosted the elevated everyday demand even higher to achieve astounding gains versus year ago. Independence Day was no exception. Meat prices were still elevated and several states rolled back their relaxation of pandemic social distancing measures. In many cases, this involved stricter in-restaurant dining capacity limits. This could have prompted everyday demand to increase for the week ending July 5 along with the holiday demand.

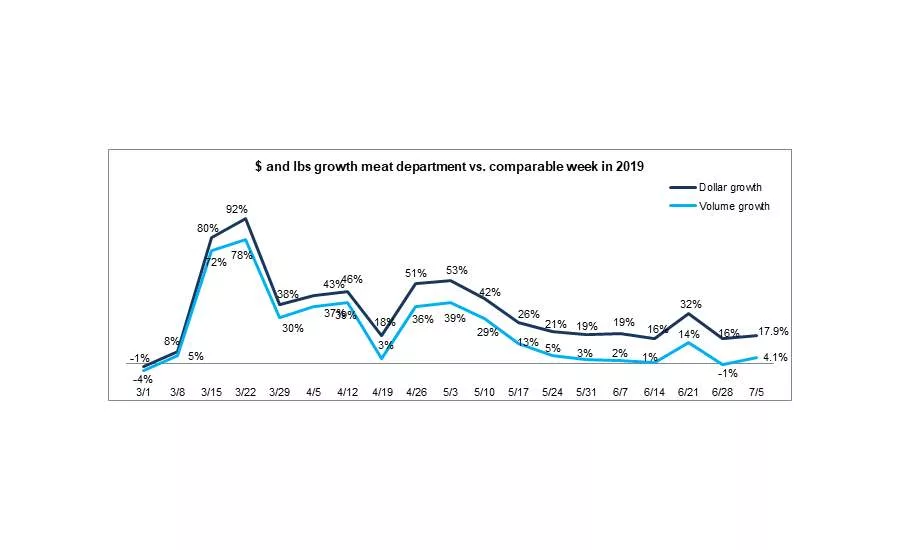

Independence Day is a much tougher holiday to beat year-over-year sales given the high focus on grilling versus eating out in regular years. However, the 2020 holiday resulted in a 17.9% increase in dollar sales versus year ago. This was the 17th week of double-digit gains since the onset of the pandemic. And while higher prices drove much of this gain, the holiday brought meat volume growth too, at +4.1%. The dollar/volume gap continued to improve to 13.8 points. Expectations for the holidays were smaller gatherings and unit sales support this assumption. Unit purchases in fresh meat increased by 8.4 million, or 5.2%, over the Fourth of July week versus last year, while volume increased 4.1%. This points to more, but smaller, packages sold.

So far during the pandemic, starting March 15 through July 5, dollar sales are up 36.4% and volume sales have increased 23.0% versus the same period last year.

Dollar versus Volume Gains

Fresh meat had a slightly stronger week than processed meat, at +19.9% in dollar gains versus +12.0%, respectively. Fresh meat also exceeded processed in volume gains. The volume/dollar gap is a little over two points wider for fresh than processed.

| Latest 1 week ending July 5, 2020 versus comparable week in 2019 | Dollar gains | Volume gains | Volume/dollar gap(percentage points) |

| Total meat | +17.9% | +4.1% | -13.8 |

| Total fresh | +19.9% | 5.4% | -14.5 |

| Total processed | +12.0% | +0.1% | -11.9 |

Source: IRI, Total US, MULO, 1 week % gain versus YA

The longer, four-week look ending July 5 also shows double-digit volume/dollar gaps for fresh beef and pork, as well as frankfurters and bacon. Despite just mild price inflation for turkey, exotic meat and ham, inflation in the much larger proteins caused a double-digit volume/dollar gap for total meat. However, prices are starting to come down with smaller differences for beef, pork and total meat compared with just a few weeks ago. Exotic meat, which includes proteins like bison, had the highest percentage gain over the four week look in both dollars and volume, but off a much smaller base.

| Latest 1 week ending July 5, 2020 versus comparable week in 2019 | Dollar gains | Volume gains | Volume/dollar gap(percentage points) |

| Total meat | +20.1% | +4.3% | -15.8 |

| Fresh beef | +25.4% | +1.4% | -24.0 |

| Ground beef | +24.3% | -0.9% | -25.2 |

| Fresh chicken | +11.7% | +3.2% | -8.5 |

| Fresh pork | +22.1% | +9.0% | -13.1 |

| Fresh turkey | +19.7% | +17.6% | -2.1 |

| Fresh lamb | +37.2% | +28.6% | -8.6 |

| Fresh exotic | +42.2% | +39.4% | -2.8 |

| Fresh veal | +18.2% | +15.7% | -2.5 |

| Smoked ham/pork | +29.6% | +26.7% | -2.9 |

| Sausage | +18.2% | +9.4% | -8.8 |

| Frankfurters | +9.4% | -7.5% | -16.9 |

| Bacon | +17.2% | +6.8% | -10.4 |

Source: IRI, Total US, MULO, 4 weeks ending July 5, 2020 versus YA

Assortment

Dipping well below 300 during the height of the supply chain woes, assortment continues to climb back up and leaped to an average of 320 items per store during Independence Day week — an increase of eight items over the prior week, though still down 28.0% versus the same week last year.

Average weekly items per store selling for week ending…

| 3/1 | 3/8 | 3/15 | 3/22 | 3/29 | April (4/5-4/26) | May (5/3-5/31) | June (6/7-6/28) | 6/28 | 7/5 |

| 335 | 334 | 353 | 330 | 308 | 315 | 301 | 304 | 312 | 320 |

Source: IRI, Total US, MULO, average weekly items per store selling

Christine McCracken, Executive Director Food & Agribusiness for Rabobank, is expecting the supply landscape to continue to improve in the upcoming weeks. “Red meat production continues to run well-ahead of year-ago levels, with pork up 9.7% and beef up 4.2%. The industry is working to restore balance following COVID-related disruption and clear up the oversupply. The increase in available meat supplies is weighing on the market, however, and may limit a sharp upturn in wholesale prices near term. Even with the larger supplies there has been a slight uptick in pork values as processors begin to prepare for the holiday ham season. Bellies were also stronger this week, as bacon inventories have worked lower and processors restore processing lines. Beef prices have also been steady, but slow to rebound. Lower prices were able to restore some feature activity, although ground beef ads remain relatively limited. Chicken continues to struggle, as production cuts taken early in the disruption appear insufficient. Boneless breast meat prices remain underwhelming and retail support for chicken failed to materialize around the July 4th holiday. Dark meat prices have also struggled, with boneless thigh meat weaker in recent days and unable to attract retail support. While chicken production for the week trailed year-ago levels by 3.8%, foodservice and retail interest is lacking. Perhaps in response, we saw weekly egg sets drop 1.1% year-over-year in the last week. Taking action now to restore a better balance in supply and demand could bode well for stronger prices by fall.

Price

While assortment and availability improved, consumers continued to call out higher meat prices and fewer meat features on the Retail Feedback Group’s Constant Customer Feedback (CCF) system. “Meat prices have increased two to three times compared with February.” Another expressed understanding, yet having trouble staying on budget. “I think this is more due to COVID crisis than the store, but definitely see an increase in prices in meat and chicken. Having a family of five with three teenagers, it is harder to stay on budget with the price increases.” Another shopper pointed to the need for more specials, “Meat prices are outrageous and keep going up each visit. Extra specials would be appreciated.”

Independence Day week typically sees several hot, traffic-driving promotions, with stores even opting for loss-leaders in some cases. This year, the holiday did not bring this type of extreme sale prices. Overall, the fresh promoted price for the holiday week this year was $3.77 versus $2.96 last year.

Aside from promotional prices, IRI’s insights on the average retail price per volume show double-digit increases when comparing to Independence Day week in 2019, however, the big three showed significant declines in price per volume versus the preceding 2020 week. Compared to the week ending June 28, beef prices were down 7.6% during the holiday week, chicken prices decreased 3.2% and pork 5.0%. Across all meats, prices were down nearly 4% compared with the prior week ending June 2020.

Average price per volume versus the same period a year ago

1 week ending July 5

| Average | Change vs. prior period | Change vs. YA | |

| Total meat | $3.92 | -3.9% | +13.2% |

| Fresh beef | $5.69 | -7.6% | +16.8% |

| Ground beef | $4.32 | -7.3% | +17.5% |

| Fresh chicken | $2.42 | -3.2% | +10.0% |

| Fresh pork | $2.85 | -5.0% | +8.8% |

| Fresh turkey | $3.41 | +0.5% | +2.8% |

| Fresh lamb | $8.56 | +0.2% | +7.6% |

| Fresh exotic | $4.56 | +5.6% | +4.4% |

4 weeks ending July 5

| Average | Change vs. year ago | |

| Total meat | $4.06 | +15.1% |

| Fresh beef | $6.16 | +23.6% |

| Ground beef | $4.74 | +25.4% |

| Fresh chicken | $2.47 | +8.2% |

| Fresh pork | $3.02 | +12.0% |

| Fresh turkey | $3.38 | +1.8% |

| Fresh lamb | $8.52 | +6.7% |

| Fresh exotic | $4.45 | +2.1% |

Source: IRI, Total US, MULO, 1 week and 4 weeks ending July 5, 2020

Meat Gains by Protein

The overall 17.9% meat department gain was fueled by double-digit gains for all proteins, with chicken improving to +10.5% for the holiday week. Lamb and beef had the highest percentage growth, at +34.1% and +23.2%. Beef easily had the highest absolute dollar gains (+$137 million), followed by pork (+$35 million) and chicken (+$26 million).

Grinds

Ground meat is proving itself during the ultimate grilling holiday with double-digit increases in dollar sales for ground beef, turkey, chicken and pork. All but beef saw double-digit volume gains as well. Ground beef gains were likely more subdued due to the inflationary conditions, with some consumers substituting with other species, including exotic meats, such as bison, which have seen an extremely strong performance these past four months.

- Ground beef increased 23.2% in dollars and saw a small improvement in volume as well, at +1.4%.

- Ground turkey, +18.9% in dollars and +15.7% in volume.

- Ground chicken, +10.6% in dollars and +15.8% in volume

- Ground pork, +21.8% in dollars and +11.9% in volume.

For the week ending July 5 versus year ago, these four ground proteins generated $316 million in sales, which represents an additional $51 million versus year ago. Ground beef represents 89.4% of these additional dollars.

The Pandemic Sales Performance by Area

Total meat department sales came in at $1.66 billion for the week of July Fourth. Growth percentages versus year ago were not as high as those seen for Father’s Day week, however, Independence Day is a tougher holiday to go up against given the at-home-grilling versus restaurant-visit tradition. All areas were in positive territory, with only Frankfurters in the mid single digits.

2020 Weekly $ sales gains versus comparable 2019 week ending…

| 3/1 | March (3/8-3/29) | April (4/5-4/26) | May (5/3-5/31) | June (6/7-6/28) | 6/28 | 7/5 | 7/5 | |

| TOTAL MEAT | -1% | +54% | +38% | +32% | +22% | +15.8% | +17.9% | $1.7B |

| Fresh | ||||||||

| Beef | 0% | +53% | +42% | +36% | +27% | +22.2% | +23.2% | $727M |

| Chicken | +1% | +41% | +32% | +21% | +13% | +6.9% | +10.5% | $273M |

| Pork | -5% | +56% | +44% | +32% | +24% | +14.6% | +21.8% | $195M |

| Turkey | 0% | +72% | +36% | +43% | +23% | +18.0% | +18.9% | $40M |

| Lamb | +1% | +34% | +8% | +36% | +39% | +30.5% | +34.1% | $10M |

| Exotic | +5% | +92% | +54% | +61% | +48% | +44.2% | +33.2% | $3M |

| Processed | ||||||||

| Smoked ham/pork | -6% | +118% | +20% | +63% | +35% | +25.6% | +26.5% | $16M |

| Sausage | 0% | +63% | +42% | +35% | +24% | +13.8% | +11.9% | $161M |

| Frankfurters | -1% | +76% | +39% | +20% | +17% | -2.1% | +5.6% | $103M |

| Bacon | -6% | +54% | +48% | +34% | +18% | +19.1% | +15.8% | $129M |

Source: IRI, Total US, MULO, 1 week % change vs. YA

Market Shifts

The strong beef dollar gains prompted its share of total dollars for the week ending July 5 to jump to 58.2% versus 53.3% pre-pandemic, the first week of March. Pork also gained significantly in dollar share, from 12.9% during the week of March 1 to 15.6% the week of July 5. Both also saw significant increases in volume share — likely related to the Holiday week with beef and pork being big grilling items. Chicken’s dollar share has been down throughout the pandemic and is down in both dollars and volume.

2020 Weekly $ sales gains versus comparable 2019 week ending…

| Share of dollar sales | Share of volume sales | |||||

| Week ending 3/1 | Week ending 7/5 | Building calendar year 2019 | Building calendar year 2020 | Week ending 3/1 | Week ending 7/5 | |

| Beef | 53.3% | 58.2% | 51.3% | 55.5% | 37.0% | 39.6% |

| Chicken | 27.5% | 21.8% | 26.6% | 25.2% | 40.5% | 34.9% |

| Pork | 12.9% | 15.6% | 13.5% | 13.7% | 16.5% | 21.3% |

| Turkey | 4.4% | 3.2% | 4.2% | 4.3% | 4.8% | 3.6% |

| Lamb | 0.9% | 0.8% | 0.9% | 0.9% | 0.4% | 0.4% |

| Veal | 0.1% | 0.1% | 0.1% | 0.1% | 0.1% | <0.1% |

| Exotic | 0.3% | 0.3% | 0.3% | 0.3% | 0.2% | 0.2% |

Source: IRI, Total US, MULO, % of total meat department dollars | “All other” not reflected

What’s Next?

Independence Day week was the last of the spring and summer holidays, leaving a seven week stretch of regular weeks where everyday demand will likely continue boost sales past last year’s levels. Wave 14 of the IRI shopper surveys shows that concern over COVID-19 is rebounding as cases rise around the country. Thirty-eight percent now say they are more concerned than they were last week and 41% of Americans are bracing for longer duration, expecting the health crisis to last at least 12 more months.

Given the rising concern and the rolling back of restaurant re-openings, foodservice meat demand may plateau, while consumers once more flock to supermarkets for their animal protein needs. It is likely that dollar gains at retail will sit above the 2019 baseline for the foreseeable future. Depending on price, volume gains may see some pressure as consumers have been diverting protein dollars to frozen meat and seafood as well as fresh seafood. Inflation in fresh and processed meats has started to moderate these past few weeks and this is expected to continue as supply is ample.

Making meal planning easy remains one of the biggest opportunities for the meat supply chain as consumers prepare an average of 84% of meals at home, according to IRI’s weekly survey. Consumers, who were initially taking to preparing more scratch meals, are running out of meal ideas and craving variety. Pre-pandemic, it was exactly this meal fatigue that drove consumers to visit restaurants and buy meal kits instead of cooking at home. Additionally, the lunch opportunity is big as 38% of those who will be working next month expect to be working from home five days per week. This is compared to 15% doing so pre-pandemic.

Source: 210 Analytics/IRI

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!