Club and grocery take above average share of pandemic meat dollars

The second full week of August was the fifth of eight non-holiday weeks between Independence Day and Labor Day, in which everyday demand alone drives sales. Consumer concern over the COVID-19 pandemic remained highly elevated and several severe weather events rendered hundreds of thousands of households along the Eastern seaboard and Midwest without power.

Additionally, economic pressure is being compounded by the delay over the extension of unemployment benefits and uncertainty over a second round of stimulus payments. IRI primary shopper research released August 11 found that that if Americans were to receive a second stimulus check from the U.S. government, they would be more likely to spend it on meat than other food and beverages. In all, 21% of consumers said they would buy more meat, 20% more produce and 7% would purchase restaurant meals more often. To the contrary, IRI also asked how the loss of a weekly unemployment benefit of $600 might affect shopping behavior. The top answer among current beneficiaries of the benefit was buy less meat at 35%, followed by buy fewer fresh fruits and vegetables at 29%, buy fewer premium products at 24%, switch more purchases to store brands vs. national brands at 19%, and buy fewer convenient meals to instead cook from scratch at 18%.

The net result of all the positive and negative forces for the meat department was double-digit dollar gains, at +14.8% during the week ending August 9 versus the comparable week year ago. While the 22nd week of double-digit dollar gains, this also marked the lowest year-over-year gain since the onset of the pandemic purchasing starting March 15. Sales gains were far below average in states affected by hurricane Isaias, due to continued power outages in Connecticut (+9.5%) and New York (+8.8%). In each, processed meat sales gains were double that of fresh. Volume gained held at 5.9%. At an average of $3.84 during the week of August 9, prices continued to move in favor of the consumer, which eroded dollar gains a little.

So far during the pandemic, starting March 15 through August 9, dollar sales are up 33.1% and volume sales have increased 20.2% versus the same period last year. This translates into an additional $8.3 billion in meat department sales during the pandemic, which includes an additional $3.8 billion for beef, $1.1 billion for chicken and $870 million for pork. Unit sales continue to do well, with 11.9 million more transactions compared with same week year ago and 868 million more transactions since the pandemic began. This continues to indicate more frequent and deep meat shopping engagement than previously seen.

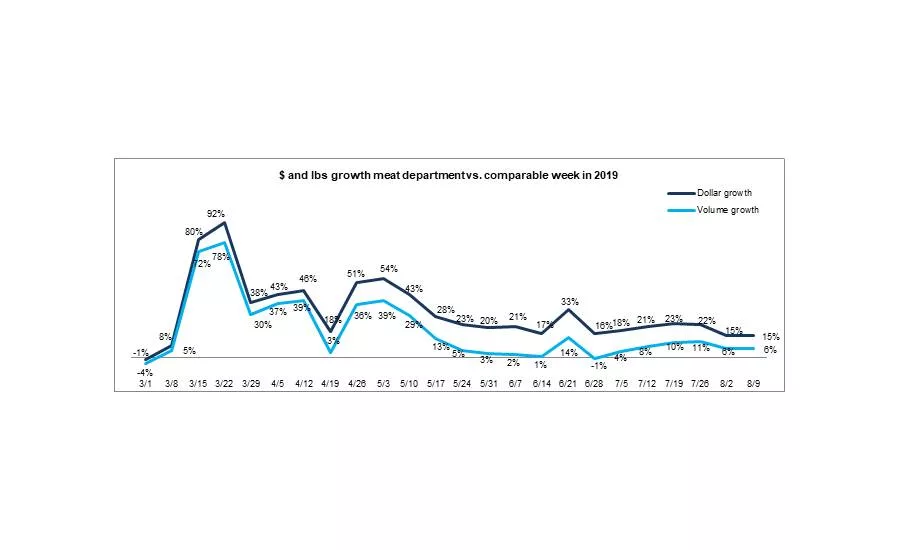

Dollar versus Volume Gains

Falling to single-digits for the first time since April 12 last week, the gap between volume versus dollar gains continued to narrow this week, at 8.9 percentage points. The volume/dollar gap was 19.1 percentage points at its widest the week of June 21st. Fresh meat (+14.7%) dollar gains were slightly stronger than processed meat (+15.2%). Fresh meat volume gains were slightly lower than those seen for processed meat.

| Latest 1 week ending August 9, 2020 versus comparable week in 2019 | Dollar gains | Volume gains |

Volume/dollar gap (percentage points) |

| Total meat | +14.8% | +5.9% | -8.9 |

| Total fresh | +14.7% | +5.7% | -9.0 |

| Total processed | +15.2% | +6.6% | -8.6 |

Source: IRI, Total US, MULO, 1 week % gain versus YA

The volume/dollar gap is still in double digits in the longer, four-week look ending August 9. However, the four-week gap narrowed from 11.9 percentage points to 10.8 points — signaling average retail prices continued to come down. The longer view shows double digit gaps for beef and lamb, but pork has narrowed to just 5.4 points, now lower than chicken. Fresh exotic meats, including bison, is the only area that saw volume gains trending ahead of dollars, creating a positive gap, at +4.4 points, up from +3.4 points the week prior. In the one-week look, all fresh meats now have single digit gaps — a pandemic first for beef. Only frankfurters were still in double-digits.

| Latest 4 weeks ending August 9, 2020 versus comparable weeks in 2019 | 4-week dollar gains | 4-week volume gains | 4 week volume/dollar gap (points) | 1 week volume/dollar gap (points) |

| Total meat | +19.3% | +8.5% | -10.8 | -8.9 |

| Fresh beef | +24.8% | +11.7% | -13.1 | -9.2 |

| Ground beef | +17.3% | +5.2% | -12.1 | -8.0 |

| Fresh chicken | +10.7% | +3.3% | -7.4 | -7.4 |

| Fresh pork | +16.0% | +10.6% | -5.4 | -0.6 |

| Fresh turkey | +14.3% | +11.8% | -2.5 | +2.5 |

| Fresh lamb | +36.0% | +25.0% | -11.0 | -7.7 |

| Fresh exotic | +34.0% | +38.4% | +4.4 | +1.6 |

| Fresh veal | +15.9% | +13.2% | -2.7 | -2.3 |

| Smoked ham/pork | +22.4% | +20.1% | -2.3 | +0.8 |

| Sausage | +18.2% | +11.6% | -6.6 | -6.7 |

| Frankfurters | +15.2% | +0.1% | -15.1 | -14.5 |

| Bacon | +19.4% | +11.8% | -7.6 | -7.1 |

Source: IRI, Total US, MULO, 4 weeks ending August 9, 2020 versus YA

Meat gains by Channel

The traditional grocery and club channels continue to see an above average share of the pandemic meat dollar. Spending on meat in the club channel is still increasing, up 1.4 percentage points since the first pandemic measurement, the four weeks ending March 22. Traditional grocery, the largest channel, had a very high share during April, when shelter-in-place mandates were in place for the majority of states. Health/Specialty grocers and discount grocery have seen a bit of a decline in their share of meat spending since the pre-pandemic period as well, ending the most recent period at just 2.0% — although had only been at 2.2% for the 4 weeks ending March.

Assortment

The number of items continued to rebound to an average of 323 items per store during the week ending August 9. With non-holiday weeks typically offering fewer items, this average is down about 17 items from prior year levels.

The vastly improved assortment levels from their June lows are being noticed by shoppers commenting on the Retail Feedback Group’s Constant Customer Feedback (CCF) system. “I have been pleased lately with the availability in the meat department. Unlike before, when I look for a meat item, it is usually in stock. Thank you.”

| Average weekly items per store selling for week ending… | ||||||

| March (3/1-3/29) | April (4/5-4/26) | May (5/3-5/31) | June (6/7-6/28) | July (7/5-7/26) | 8/2 | 8/9 |

| 332 | 315 | 301 | 304 | 317 | 320 | 323 |

Source: IRI, Total US, MULO, average weekly items per store selling

Price

The Retail Feedback Group’s Constant Customer Feedback (CCF) system continued to capture price-related comments. One shopper wrote, “I understand prices in most food areas are increasing, especially during these times, but the prices on some of the meat products were incredibly high. Is there something that can be done?”

Another shopper noted, “Seafood prices are too high for being one small state away from the ocean and specials on meat are not what they used to be but at least getting better.”

IRI insights on the price per volume shows prices are indeed still elevated but coming down, with the exception of chicken and pork prices that were up slightly. However, the year-over-year comparison shows that pork prices were virtually back in line with 2019 levels the week of August 2. Beef prices were still the most elevated versus year ago, but also down to single digits. In the longer four-week look, beef’s year-over-year prices were still in double-digits, including ground beef prices. Chicken is the only protein that has a higher year-over-year increase in the one-week look versus the four-week look.

|

Average price per volume versus the same period year ago |

1 week ending August 9 | 4 weeks ending August 9 | ||||||||||

| Average | Change vs. prior period |

Change vs. YA |

Average | Change vs. year ago | ||||||||

| Total meat (fresh + processed) | $3.84 | -1.0% | +8.4% | $3.89 | +9.9% | |||||||

| Fresh beef | $5.39 | -3.6% | +8.3% | $5.58 | +11.7% | |||||||

| Ground beef | $4.12 | -3.6% | +7.8% | $4.26 | +11.5% | |||||||

| Fresh chicken | $2.47 | +1.1% | +7.6% | $2.47 | +7.1% | |||||||

| Fresh pork | $2.77 | +1.6% | +0.6% | $2.81 | +4.8% | |||||||

| Fresh turkey | $3.26 | -6.1% | -2.2% | $3.37 | +2.2% | |||||||

| Fresh lamb | $8.42 | -2.1% | +6.6% | $8.57 | +8.8% | |||||||

| Fresh exotic | $4.26 | +0.6% | -1.3% | $4.24 | -3.1% | |||||||

| 2020 Weekly $ sales gains versus comparable 2019 week ending… | $ | |||||||||||

| 3/1 |

March (3/8-3/29) |

April (4/5-4/26) |

May (5/3-5/31) | June (6/7-6/28) | July (7/5-7/26) | 8/2 | 8/9 | 8/9 | ||||

| TOTAL MEAT | -1% | +54% | +38% | +32% | +22% | +21% | +15.4% | +14.8% | $1.33B | |||

| Fresh | ||||||||||||

| Beef | 0% | +53% | +42% | +36% | +27% | +28% | +20.2% | +20.6% | $570M | |||

| Chicken | +1% | +41% | +32% | +21% | +13% | +12% | +7.9% | +4.0% | $249M | |||

| Pork | -5% | +56% | +44% | +32% | +24% | +21% | +12.3% | +12.4% | $130M | |||

| Turkey | 0% | +72% | +36% | +43% | +23% | +17% | +8.6% | +12.5% | $39M | |||

| Lamb | +1% | +34% | +8% | +36% | +39% | +39% | +30.6% | +24.3% | $9M | |||

| Exotic | +5% | +92% | +54% | +61% | +48% | +36% | +31.6% | +29.5% | $3M | |||

| Processed | ||||||||||||

| Smoked ham/pork | -6% | +118% | +20% | +63% | +35% | +26% | +16.3% | +19.2% | $16M | |||

| Sausage | 0% | +63% | +42% | +35% | +24% | +17% | +14.4% | +15.3% | $125M | |||

| Frankfurters | -1% | +76% | +39% | +20% | +17% | +14% | +11.2% | +13.0% | $59M | |||

| Bacon | -6% | +54% | +48% | +34% | +18% | +19% | +16.4% | +15.4% | $117M | |||

Source: IRI, Total US, MULO, 1 week % change vs. YA

Grinds

Ground beef’s performance improved slightly versus the week prior. Both dollar and volume gains saw some improvement, with volume gains back in the plus. Ground turkey gains remained in single digits, but improved slightly nonetheless.

- Ground beef increased 11.8% in dollars and volume came back to positive territory, at +3.7%

- Ground turkey, +9.3% in dollars and +7.9% in volume

- Ground chicken, +17.5% in dollars and +14.5% in volume

- Ground pork, +9.8% in dollars and +7.4% in volume

Combined, these four ground proteins generated $243 million in sales, up from $232 million the week prior. Ground beef represented 86.9% of these additional year-over-year dollars.

Market Shifts

The pandemic market share trends remained unchanged in early August. Beef and pork had a higher dollar and volume share than pre-pandemic. Exotic meats, which includes bison, are the third protein with volume gains. Pork, in particular, has seen an uptick in volume share, from 16.5% during the first week of March to 17.6% the week ending August 9. Chicken and turkey remained down in both dollar and volume share.

| Share of dollar sales | Share of volume sales | |||||

| Week ending 3/1 | Week ending 8/9 | Building calendar year 2019 | Building calendar year 2020 |

Week ending 3/1 |

Week ending 8/9 |

|

| Beef | 53.3% | 57.0% | 54.2% | 55.5% | 37.0% | 39.6% |

| Chicken | 27.5% | 24.9% | 26.8% | 25.3% | 40.5% | 37.7% |

| Pork | 12.9% | 13.0% | 13.5% | 13.6% | 16.5% | 17.6% |

| Turkey | 4.4% | 3.9% | 4.2% | 4.3% | 4.8% | 4.4% |

| Lamb | 0.9% | 0.9% | 0.9% | 0.9% | 0.4% | 0.4% |

| Veal | 0.1% | 0.1% | 0.1% | 0.1% | 0.1% | <0.1% |

| Exotic | 0.3% | 0.3% | 0.3% | 0.3% | 0.2% | 0.3% |

Source: IRI, Total US, MULO, % of total meat department dollars | “All other” not reflected

What’s Next?

Consumer concern over COVID-19 remains high but stable. Everyday spending on groceries, including meat, will increasingly depend on shoppers’ individual financial situation as economic pressure and uncertainty is mounting. Back-to-school season is in full swing, though it looks very differently from prior years in most states. This will continue to impact year-over-year trend lines, particularly for meats affected by breakfast and lunch occasions with many more children at home while participating in virtual education.

Between the continued social distancing mandates, highly elevated consumer concern about the virus, economic pressure and the impact of virtual schooling, meat sales are likely to remain highly elevated for the foreseeable future.

Source: 210 Analytics/IRI

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!