Beef dazzles in strong meat department Labor Day performance

Already a strong grocery holiday during regular times, expectations for Labor Day grocery sales were high and reality did not disappoint. The holiday fell a week later than in 2019, which helped further boost the results in departments across the store, including the meat department.

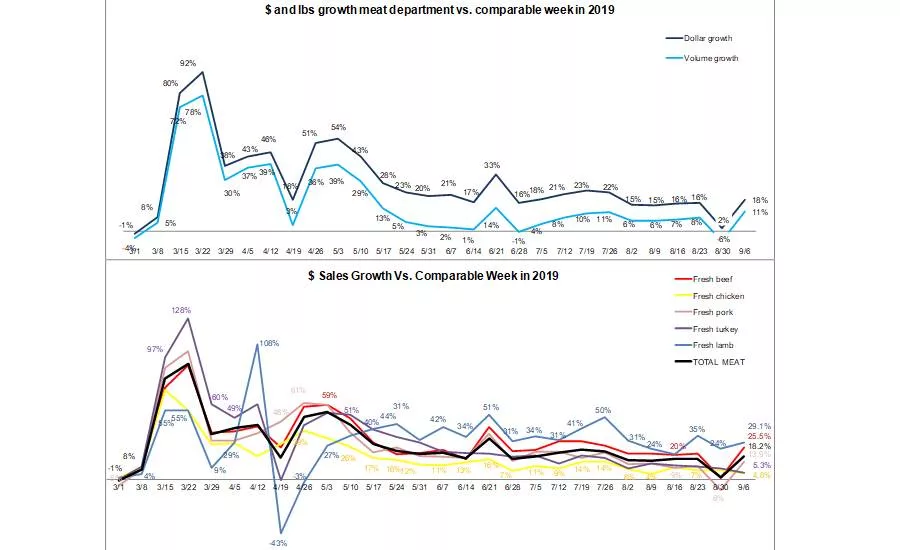

Following its first single-digit gain since the onset of the pandemic last week, the meat department bounced back strongly. For the week ending September 6, dollars gained 18.2% over year ago levels during one of the biggest grilling weekends of the summer. Volume gains jumped into double digits as well, at +11.4%. The week of September 6th had 11.2% more transactions compared to same week year ago. These results were positively influenced by the off-timing between the 2020 and 2019 holidays. However, if we were to compare the holiday weeks against one another directly, the 2020 performance remains impressive, up 15.9% in dollars and +8.5% in volume.

So far during the pandemic starting March 15 through September 6, overall meat dollar sales are up 30.1% and volume sales have increased 18.0% versus the same period last year. This translates into an additional $8.9 billion in meat department sales during the pandemic, which includes an additional $4.1 billion for beef, $1.2 billion for chicken and $909 million for pork than the same period in 2019.

Dollar versus Volume Gains

The gap between dollar gains and volume gains narrowed further, now reaching 6.8 percentage points — the smallest gap since mid-April and down from 19.1 points during the week of June 21st. Processed meat had the strongest gains, up 19.9%, edging out fresh meat that gained 17.6% versus year ago levels. Processed meat also had slightly stronger volume gains.

| Latest 1 week ending September 9, 2020 versus comparable week in 2019 | Dollar gains | Volume gains |

Volume/dollar gap (percentage points) |

| Total meat | +18.2% | +11.4% | -6.8 |

| Total fresh | +17.6% | +11.2% | -6.4 |

| Total processed | +19.9% | +11.9% | -8.0 |

Source: IRI, Total US, MULO, 1 week % gain versus YA

Price per Volume and Volume/Dollar Gap

According to the IRI insights on the price per pound volume, prices continued to drop in favor of the consumer, with an average of $3.71 per volume across all meats during the week of September 6 versus $3.76 the week prior.

Retailers invested in price during the Labor Day weekend, with ground beef, chicken, pork, turkey and exotic meats (including bison) all right around last year’s pricing levels. Only beef (other than ground beef) and lamb continued to have higher levels of inflation.

The big grilling powerhouse meats, including beef and pork, all had very strong weeks. Beef increased more than 25% in dollars and 19% in volume versus the same week year ago. Smaller proteins, including lamb and exotic meats continue to have strong sales gains during holiday and everyday demand weeks — perhaps signaling that some of the protein switching seen during the weeks of tight supply are here to stay.

|

Average price per volume versus the same period year ago |

1 week ending 9/6 | Volume vs. dollar gains w.e. 9/6 | |||

| Average | Change vs. prior period |

Change vs. YA |

Dollar gains vs. YA |

Volume gains vs. YA |

|

| Total meat (fresh + processed) | $3.71 | -1.1% | +6.1% | +18.2% | +11.4% |

| Fresh beef | $5.13 | -3.4% | +5.5% | +25.5% | +19.0% |

| Ground beef | $3.78 | -7.7% | +0.7% | +11.1% | +10.3% |

| Fresh chicken | $2.38 | -2.9% | +2.1% | +4.8% | +2.7% |

| Fresh pork | $2.66 | -1.5% | -0.4% | -13.9% | +14.4% |

| Fresh turkey | $3.38 | +0.6% | +2.2% | +5.3% | +3.0% |

| Fresh lamb | $8.47 | +3.0% | +7.3% | +29.1% | +20.2% |

| Fresh exotic | $4.32 | +1.8% | -0.1% | +26.5% | +26.6% |

Source: IRI, Total US, MULO, 1 week % gain versus YA

Christine McCracken, Executive Director for Animal Protein for Rabobank, provided insight into price and harvest developments in pork. “Pork prices started to rebound in the week leading up to Labor Day as news of the first German case of African Swine Fever in a wild boar was confirmed. U.S. pork prices moved 4% higher, as leading importers in China, Japan and South Korea quickly moved to block German pork imports as they do not yet recognize World Health Organization regionalization principles. Germany is the world's fifth largest exporter of pork and a leading supplier to China. U.S. pork production averaged 7% above year-ago levels in the weeks before the holiday-shortened week, limiting prices in recent weeks. Labor remains an issue in many plants and may limit harvest levels in coming weeks. Tighter domestic supplies could boost pork prices through year-end.”

McCracken also commented on chicken and beef. “Chicken prices remain relatively flat, with the exception of wings which continue to outperform as foodservice demand remains stout. Boneless breast meat prices remain weak and are frequently discounted, as supplies remain large and foodservice demand has been unable to clear supplies. Reported disruption at some U.S. plants has not slowed RTC chicken production (up 3.7% in the last month) as heavier bird weights more than offset lower total slaughter. Cattle harvest moved lower on the holiday shortened week and has averaged down 1% for much of August. Beef supplies remain steady, with most plants operating near full capacity and expected to continue production at or above year-ago through the balance of the fall. Beef prices fell slightly in the days leading up to Labor Day, as large supplies of lower cost proteins, strong imports and weaker foodservice demand continue to limit near term upside.”

Assortment

Retailers invested in price and assortment during the Labor Day week. The average number of items leaped from an average of 324 during August to 330 per store during the holiday week. Whereas the average number of items has been off by about 17, this resulted in being down only nine items from year ago levels.

| Average weekly items per store selling for week ending… | ||||||

| March (3/1-3/29) | April (4/5-4/26) | May (5/3-5/31) | June (6/7-6/28) | July (7/5-7/26) | August (8/2-8/30) | 9/6 |

| 332 | 315 | 301 | 304 | 317 | 324 | 330 |

Meat Gains by Protein

All proteins saw robust recovery from the down week at the end of August. Pork, in particular, turned around its performance from -8% to +13.9% as a popular grilling protein. Lamb continued to lead in growth percentage; however, this is off a small base. Beef, the largest of the protein, had the second highest growth, at +25.5%. This translated into an additional $123.4 million for beef, far ahead of number two, pork, that generated an additional $17.7 million in sales versus year ago levels. Chicken was a distant third with an additional $11.4 million sold.

The Pandemic Sales Performance by Area

Meat department sales were $1.398 billion during the week of September 6 — about $168 million higher than the week prior for a week-over-week gain of 13.7%. On the fresh side, beef accounted for 57.1% of dollars. Chicken was next at 23.6% of dollars. Processed meats had a very strong Labor Day week as well. Hot dogs ended the summer season on a very high note with dollars up 28.0% versus year ago levels.

| 2020 Weekly $ sales gains versus comparable 2019 week ending… | $ | ||||||||||

| 3/1 |

March (3/8-3/29) |

April (4/5-4/26) |

May (5/3-5/31) | June (6/7-6/28) | July (7/5-7/26) | August (8/2-8/30) | 9/6 | 9/6 | |||

| TOTAL MEAT | -1% | +54% | +38% | +32% | +22% | +21% | +12.7% | +18.2% | $1.4B | ||

| Fresh | |||||||||||

| Beef | 0% | +53% | +42% | +36% | +27% | +28% | +16.3% | +25.5% | $607M | ||

| Chicken | +1% | +41% | +32% | +21% | +13% | +12% | +7.4% | +4.8% | $250M | ||

| Pork | -5% | +56% | +44% | +32% | +24% | +21% | +6.8% | -13.9% | $144M | ||

| Turkey | 0% | +72% | +36% | +43% | +23% | +17% | +10.2% | +5.3% | $37M | ||

| Lamb | +1% | +34% | +8% | +36% | +39% | +39% | +26.6% | +29.1% | $8.5M | ||

| Exotic | +5% | +92% | +54% | +61% | +48% | +36% | +28.2% | +26.5% | $2.9M | ||

| Processed | |||||||||||

| Smoked ham/pork | -6% | +118% | +20% | +63% | +35% | +26% | +14.8% | +10.6% | $16M | ||

| Sausage | 0% | +63% | +42% | +35% | +24% | +17% | +13.2% | +18.7% | $133M | ||

| Frankfurters | -1% | +76% | +39% | +20% | +17% | +14% | +9.7% | +28.0% | $67M | ||

| Bacon | -6% | +54% | +48% | +34% | +18% | +19% | +15.2% | +18.2% | $119M | ||

Source: IRI, Total US, MULO, 1 week % change vs. YA

Grinds

As a holiday powerhouse, ground beef experienced double-digit gains in both dollars and volume after a tough week at the end of August. Ground beef far outperformed the other grinds that mostly experienced single-digit increases versus year ago levels.

- Ground beef increased 11.1% in dollars and improved 10.3% in volume

- Ground turkey increased 2.7% in dollars and +2.0% in volume

- Ground chicken, +11.0% in dollars and +11.4% in volume

- Ground pork, +7.2% in dollars and +7.0% in volume

Market Shifts

The strength of beef and pork throughout the pandemic have resulted in a gain in market share when comparing the share of dollars during the week ending March 1 versus that during the week of September 6. Both have gained significantly in dollar and volume share. Chicken, while having the second-highest share, dropped several points in both dollar and volume shares.

| Share of dollar sales | Share of volume sales | |||

| Week ending 3/1 | Week ending 9/6 | Week ending 3/1 | Week ending 9/6 | |

| Beef | 53.3% | 57.7% | 37.0% | 40.7% |

| Chicken | 27.5% | 23.8% | 40.5% | 36.1% |

| Pork | 12.9% | 13.7% | 16.5% | 18.7% |

| Turkey | 4.4% | 3.6% | 4.8% | 3.8% |

| Lamb | 0.9% | 0.8% | 0.4% | 0.3% |

| Veal | 0.1% | 0.1% | 0.1% | <0.1% |

| Exotic | 0.3% | 0.3% | 0.2% | 0.2% |

Source: IRI, Total US, MULO, % of total meat department dollars | “All other” not reflected

Category Engagement

July and August continued to see elevated levels of household penetration, trips and spend per buyer versus year ago levels for the Meat department, including both fixed and random weight. These were all weeks where everyday demand carried the year-over-year gains, which means the meat department won in every area of growth from sales to shoppers and beyond.

| Total meat | Buyers | Trips | Dollars per trip | |||

| Week ending 3/1 | Week ending 9/6 |

Week ending 3/1 |

Week ending 9/6 |

Week ending 3/1 |

Week ending 9/6 |

|

| w.e. 07/12 | 74.6M | +6.2% | 1.5 | +1.2% | $15.03 | +14.3% |

| w.e. 07/19 | 75.0M | +7.7% | 1.6 | +2.0% | $14.88 | +13.7% |

| w.e. 07/26 | 74.6M | +7.3% | 1.5 | +2.3% | $14.61 | +12.8% |

| w.e. 08/02 | 72.2M | +3.7% | 1.5 | +0.7% | $15.00 | +12.7% |

| w.e. 08/09 | 74.1M | +2.3% | 1.6 | +1.7% | $14.87 | +11.2% |

| w.e. 08/16 | 74.2M | +4.3% | 1.6 | +1.8% | $14.42 | +10.0% |

| w.e. 08/23 | 72.9M | +4.1% | 1.5 | +2.3% | $14.52 | +11.1% |

Source: IRI household panel data, All Outlets, Meat Department (fixed and random weight, fresh and processed, does not include Frozen)

What’s Next?

This is the last in the weekly series of meat performance reports IRI and 210 Analytics have produced since the week of March 15, after which the reports will continue on a monthly basis.

Excluding weeks that were affected by the 2019 or 2020 holiday demand, everyday demand is normalizing at around 10%-15% above year ago levels, depending on how price inflation will impact dollar sales. The number of new COVID-19 cases appears to be leveling off and consumer concern along with it. Restaurant transactions continue to come back a little at a time, but remain below year-ago levels. Aided by the effect of virtual schooling and working-from-home, meat sales are likely to hold well above 2019 levels for many weeks to come.

Source: 210 Analytics/IRI

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!