Lamb and smoked ham post strong sales leading up to Easter

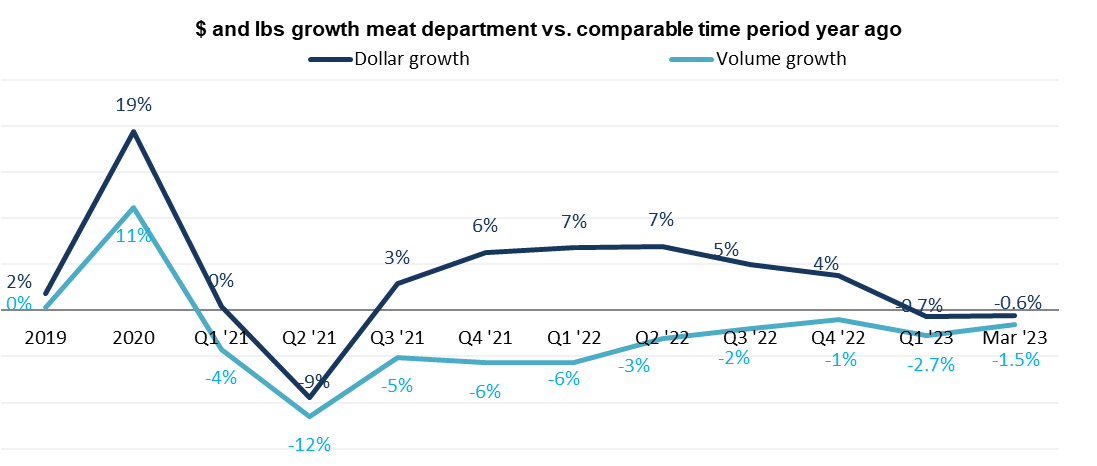

March meat sales stayed within 1.5% of last year’s level in pounds, while dollars sales were virtually flat at -0.6%.

The March marketplace

For the first time in many months, inflation for total food and beverages stayed in the single digits. The March 2023 average price per unit across all foods and beverages and channels increased 9.8% over March 2022, but sat 21.43% above the March 2021 and 27.4% above the March 2020 levels. Salaries are not keeping pace and the grocery marketplace continues to be in flux as consumers move around dollars between channels, products and brands. Circana (formerly IRI), 210 Analytics and Hillphoenix are teaming up to bring you the latest in grocery retailing and meat department sales and trends.

The Bureau of Labor Statistics reported that March restaurant prices increased 8.4%. Major metropolitan areas such as Detroit, Dallas and Philadelphia, have experienced far greater food and beverage inflation, per the BLS.

- The U.S. Government Accountability Office reported that low-income households spend an average of 30% of their total income on food. Low-income households over index for the share of meals prepared at home, at an estimated 79.8% of all meals, per the March Circana survey, versus 74.2% for those making $100,000 or more annually.

- Per the Circana survey, 94% of primary shoppers are concerned about the price increases and preparing meals at home remains one of the chief measures in addition to looking for sales specials and buying private brands.

The 2022 record, double-digit gains in store brands seemed to be a tough act to follow. However, the first quarter 2023 shows continued private brand growth with dollar sales up 10.3% across items and channels, twice the gain of national brands that grew 5.6%. The dollar share of private brands rose to 19.1% and the unit share to 20.8%.

- Double-digit gains in store-brand sales included several fresh departments including bakery (+17.0%), refrigerated (+15.5%) and deli-prepared foods (+12.4%).

- In the meat department, national brands outperformed private label in the first quarter of 2023. Private brands, that reflect 44% of total first quarter meat sales, were down 1.7% in dollars sales versus the first quarter of 2022. Manufacturer brands reflected 56% of sales and were down a mere 0.6% in dollar sales.

The online grocery market in March posted $8.0 billion in total sales, down 7.6% compared to last year, according to Brick Meets Click. All three areas of delivery, pickup and ship-to-home declined year-on-year.

Inflation insights

The price per unit across all foods and beverages in the Circana-measured multi-outlet stores, including supermarkets, club, mass, supercenter, drug and military, increased 9.8% in March (the five weeks ending 4/2/2023), which was down from 11.2% in February and +13.2% in January 2023.

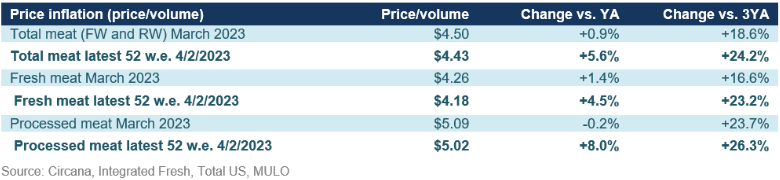

The average price per pound in the meat department across all cuts and kinds, both fixed and random weight, stood at $4.50 in March 2023. Prices only increased slightly year-on-year, at +0.9% — continuing a trend of moderating levels.

By protein, March prices decreased for beef, pork, lamb, bacon and smoked ham when compared to March 2022. Only packaged lunchmeat had double-digit inflation, whereas price increases in chicken and turkey have started to moderate.

Meat sales

March meat sales stayed within 1.5% of last year’s level in pounds. In dollars, sales were virtually flat at -0.6%. Fresh meat was the biggest seller and outperformed processed meat in dollars and pounds.

Both dollar and pound sales trend around year ago levels in March 2023 but a tough January pulled down the results for the entire first quarter of the year.

Assortment

Assortment

Assortment, measured in the number of weekly items per store is averaging 491 meat and poultry SKUs. Levels are holding steady against the 2022 averages, but remain down substantially against 2019.

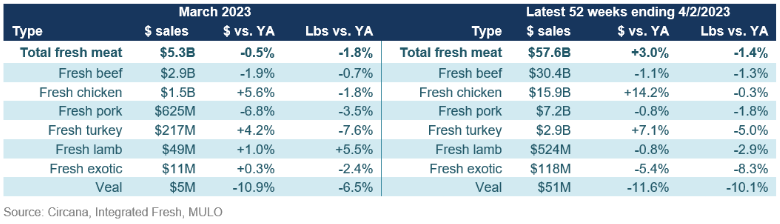

Fresh meat sales by protein

In all, the combination of mild inflation with subdued volume pressure prompted a -0.5% decrease in fresh meat sales in March 2023 versus March 2022. Beef was the biggest seller and lamb was the only one to grow dollars and pounds in March.

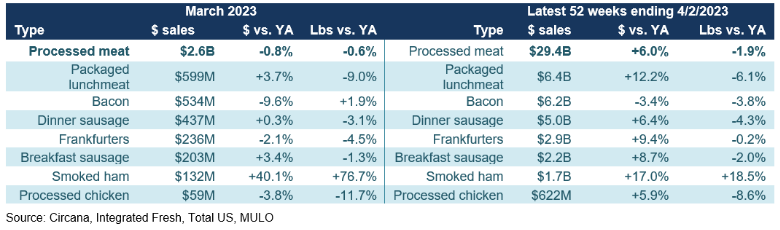

March processed meat sales remained right around year ago levels in both dollars and pounds. Smoked ham pulled sharply ahead of March 2022, likely due to the different timing of Easter between the two years. Packaged lunchmeat, dinner sausage and processed chicken grew dollars, but lost ground in pounds.

In the 52-week view, dollar sales did remain ahead of year ago levels, but pound sales trailed by 1.9%. Aside from smoked ham trending ahead, Frankfurters came closest to matching last year’s pound sales, at -0.2%.

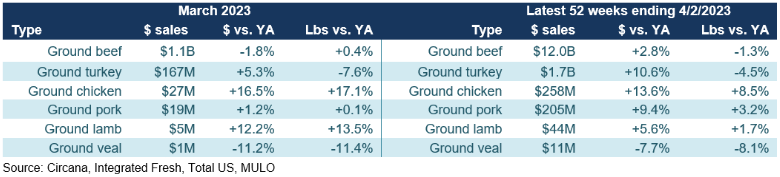

Grinds

In the past year, grinds generated $14.2 billion, with 85% of dollars and pounds being generated by ground beef. The ground beef performance exceeds that of total beef, with pounds down a mere -1.3% over the full-year view and up year-on-year in March. Additionally, ground chicken, pork and lamb gained in pounds in March as grinds bring affordability and versatility to the meat department.

What’s next?

Circana’s monthly shopper survey looked ahead to the kick off of grilling season:

- 56% of consumers tend to do something special for Memorial Day, led by getting together with friends and family (27%), cookouts (20%), outdoor activities, travel, parties and more.

The meal preparation landscape continues to change as well.

- 82% of consumers bought food from restaurants in the past few weeks, with an uptick in the share who have dined on premise to 52%, edging out takeout, at 51%.

- 19% of shoppers in the Circana survey believe they will cook meals from scratch more often versus 5% less often. The primary drivers for wanting to cook meals from scratch more often are saving money (68%) and eating healthier meals (59%). Those looking to dial back scratch cooking cite lack of time as their primary reason.

The next performance report in the Circana, 210 Analytics and Hillphoenix series will be released mid-May 2023 to cover the April sales trends.

Please thank the entire meat and poultry industry, from farm to store, for all they do.

Date ranges

2019: 52 weeks ending 12/28/2019

2020: 52 weeks ending 12/27/2020

2021: 52 weeks ending 12/26/2021

2022: 52 weeks ending 1/1/2023

Q4 2022: 13 weeks ending 1/1/2023

Q1 2023: 13 weeks ending 4/2/2023

March 2023: 5 weeks ending 4/2/2023

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!