State of the Industry

State of pork: Looking forward

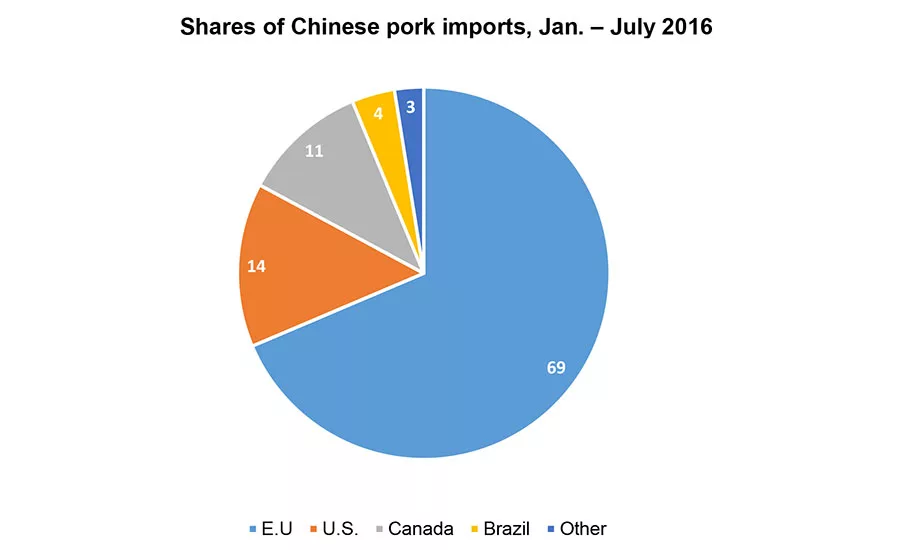

For the U.S. to displace Europe as a predominant export partner for China in the future, the industry will need to remove the drug from animal diets.

Pork is the third most popular protein among U.S. consumers; however, it is the most consumed protein on the planet. As global demand continues to rise, there are significant future opportunities for U.S. pork exports, which are projected to total 20 percent of domestic production in 2016.

Pork exports lag slightly behind the prior year, predominantly because of the effects of a strong U.S. dollar. It is therefore surprising that, even with the price-sensitive nature of many leading export markets such as Mexico, shipments haven’t declined at a faster pace. Nonetheless, with pork supplies expected to rise in the second half of 2016 due to increased slaughter, a more stable price environment should be supportive of exports.

The impact of export shortfalls to Mexico, Japan and South Korea have been offset by the increase in exports to China. In fact, despite the economic slowdown, China has more than doubled its pork consumption from the U.S. this year. China should continue to be a popular destination for U.S. pork going forward, particularly if domestic producers continue to move away from the use of ractopamine as a feed additive. Many countries around the world, including China, ban the use of this additive in livestock. For the U.S. to displace Europe as a predominant export partner for China in the future, the industry will need to remove the drug from animal diets.

This is a timely issue for the broader pork market in the context of the antibiotic-free (ABF) movement occurring within the protein industry. This has been promoted aggressively in the chicken industry as a result of several leading quick-service restaurant chains converting to ABF production and promoting the changes to drive marketing and brand differentiation.

Whether consumers truly want this change, and the associated price increases, is yet to be determined. There is no denying, however, that the foodservice establishment, followed closely by food retailers, is causing noticeable ripple effects in the protein supply chain with this push to ABF.

It will be interesting to see how the U.S. pork industry reacts to the bans on ractopamine given the potential for headwinds within an export market that has buoyed the industry in recent years. It will be equally important to observe the pace at which an ABF platform for pork develops within domestic distribution channels.

In the interim, live hog supplies are robust due partly to increases in sow farrowing but mostly as a result of the remarkable gains in efficiencies as evidenced by continuing increases in litter rates. According to the recent USDA report for the March-May swine herd, we’re at a 45-year high in the size of the pig crop. In addition, the record high level of market hog inventories reported on June 1 suggests we can expect to see a seasonal uptick in pork production in the latter half of the year. But overall production increases for 2016 remain fairly modest.

These factors support the view that live hog prices should remain reasonably low and that modest improvements in wholesale pork prices will boost packer profitability heading into 2017. NP

State of the Industry 2016 segments

| Industry overview | Goes live Oct. 14 |

| Beef (CAB) | Oct. 18 |

| Beef (NCBA) | Oct. 19 |

| Pork (Pork Board) | Oct. 20 |

| Pork (Sun Trust) | Oct. 21 |

| Chicken | Oct. 24 |

| Turkey | Oct. 25 |

| Veal | Oct. 26 |

| Lamb | Oct. 27 |

| Food Safety | Oct. 28 |

| Packaging | Oct. 31 |

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!