State of the Industry

State of lamb: On the road to growth

American lamb is a prominent protein in upscale restaurants, appearing on 65 percent of fine-dining menus.

Per capita consumption of lamb in the U.S. has remained steady over the past 10 years at approximately one pound per year.

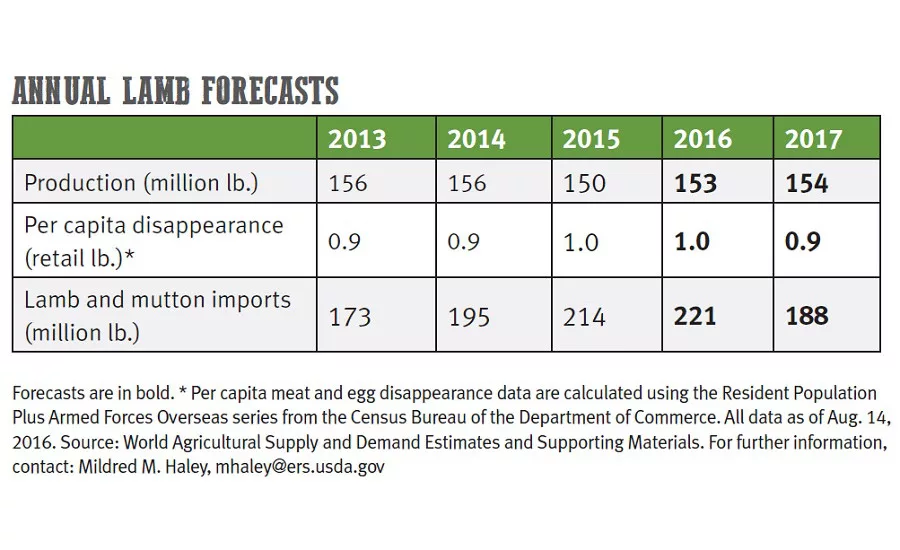

Approximately 300 million pounds of lamb are sold each year in the United States, with lamb imports from Australia and New Zealand now representing over half the total lamb supplies. Per capita consumption of lamb in the U.S. has remained steady over the past 10 years at approximately one pound per year. The highest consumption of lamb in the U.S. occurs in the northeast and southeast regions, and in the state of California. Roughly 40 percent of lamb is sold into foodservice while the other 60 percent is sold into retail.

There are opportunities for lamb consumption to expand, and the lamb industry is working at growing its footprint. For instance, roughly 40 percent of consumers have never eaten lamb, and many consumers link lamb primarily to special occasions and eating out. Minority populations consume more than 50 percent of the lamb sold in the U.S., and the average lamb household spends 30 percent more per year on food than the average household.

Retail

According to IRI Freshlook Marketing Data, lamb retail sales (pounds sold) were up 6 percent for the 52 week period ending July 10, 2016. Leg, shoulder and loin are the top-selling lamb cuts at retail (67 percent of total lamb sold). As more and more consumers look for lamb and want affordable and easy to prepare cuts, ground lamb sales continue to grow and now represent 10 of total lamb sales and pounds sold at retail.

Foodservice

American lamb is a prominent protein in upscale restaurants, appearing on 65 percent of fine-dining menus. Lamb is also one of the fastest growing proteins on chain and independent dining menus. According to a recent study, Datassential MenuTrends, lamb items on independent and chain restaurant menus are up 11 percent in the last four years. Lamb continues to find growth outside of traditional center of the plate and chop offerings including burgers, pizza, sandwiches, and ethnic dishes.

Following the map

The Lamb Industry Roadmap Project was created in 2014 to bring all sectors of the industry together to identify and analyze the major challenges facing the American lamb industry. The most effective solutions and a strategy were developed in order to strengthen the short-term and long-term competitive advantage of the industry, and to return it to consistent profitability. An advisory group was appointed to guide this project, and input was gathered from all sectors of the industry. Large and small producers from all parts of the country, feeders, processors, direct marketers, the pure-bred and show industries, researchers and large industry organizations, retailers and foodservice operators were all included in the research and feedback process. Input was used from all parts of the American lamb industry in order to create a comprehensive plan to implement change.

The Roadmap promotes four major goals:

- Product Characteristics: reduce fat content and improve consistency

- Demand Creation: achieve an increase in demand for American Lamb

- Productivity Improvement: achieve a significant increase in industry productivity

- Industry Collaboration: work toward a common industry goal of meeting consumer desires.

A Roadmap Implementation Committee representing all sectors of the industry and all national industry organizations continues to work on challenges and opportunities to address these goals. NP

State of the Industry 2016 segments

| Industry overview | Goes live Oct. 14 |

| Beef (CAB) | Oct. 18 |

| Beef (NCBA) | Oct. 19 |

| Pork (Pork Board) | Oct. 20 |

| Pork (Sun Trust) | Oct. 21 |

| Chicken | Oct. 24 |

| Turkey | Oct. 25 |

| Veal | Oct. 26 |

| Lamb | Oct. 27 |

| Food Safety | Oct. 28 |

| Packaging | Oct. 31 |

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!