Meat sales maintain strong start for 2024

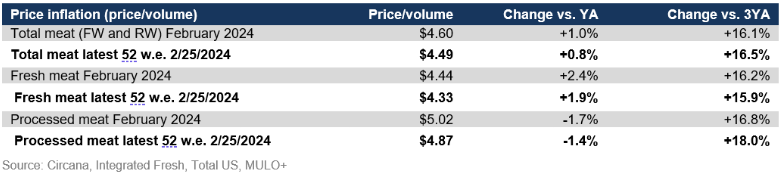

The average price per pound in the meat department across all cuts and kinds stood at $4.60 in February 2024, up 1% year-on-year.

Reversing course after three consecutive months of gains, the February consumer confidence index by the University of Michigan decreased to 76.9. Slipping two points below January, most index readings did remain substantially higher than those reported last fall as consumers remained somewhat optimistic about inflation continuing on a more favorable trajectory.

February counted several large sales events. According to the February Circana survey among primary shoppers, these occasions provided additional touchpoints for retailers in departments around the store.

- In early February, 56% of consumers expected they would watch the Super Bowl. Only 2% anticipated going to a bar or restaurant to watch the game. Among those watching the game at home, the anticipated retail spend averaged $36 on game-time snacks, beverages and food. One in five consumers planned to order takeout, such as pizza, for the game — another convenient meal sales opportunity for departments such as frozen and deli-prepared.

- As of early February, the survey found that a similar number anticipated celebrating Valentine’s Day this year, with chocolate and candy being the most common purchase, followed by cooking a special meal at home. Valentine’s Day, Mother’s Day and other big holidays that were large restaurant occasions pre-pandemic continue to see more home-centric celebrations. Shopping patterns have largely shifted back to the week in advance of the holiday.

February restaurant engagement was down from January, with 73% of consumers having dined at restaurants or ordered takeout or delivery, according to the Circana survey. The drop in restaurant visits came hand-in-hand with an increase in the estimated share of home-cooked meals as a percentage of all meals, at 79.1%.

Circana and 210 Analytics will continue to track the trends in the meat department throughout 2024 as continues shift their dollars across items, brands, sizes, stores and restaurants. The report is made possible by Hillphoenix.

Circana market expansion to MULO+

Circana has expanded the Multi-Outlet universe to include additional retailers that were previously not represented nor projected. This new geography, called MULO+, is used as of this February report for the monthly updates. The additional retailers represent e-Commerce, grocery, club, DTC delivery and other channels, fueling an average expansion of 15% across total CPG. All time period history and geographies have been updated to represent the new MULO+ universe. You will find more detailed information at the end of this report.

Inflation insights

In February 2024 (the four weeks ending 2/25/2024), the price per unit across all foods and beverages in the Circana MULO+ universe increased by 1.5% versus February 2023. Prices in the fresh perimeter were flat (+0.2%), whereas center-store grocery prices increased by 2.7%. Due to the cumulative impact of several years of high inflation, 94% of consumers in the Circana survey remained concerned over grocery prices. The February prices across food and beverages were 35% higher than they were pre-pandemic.

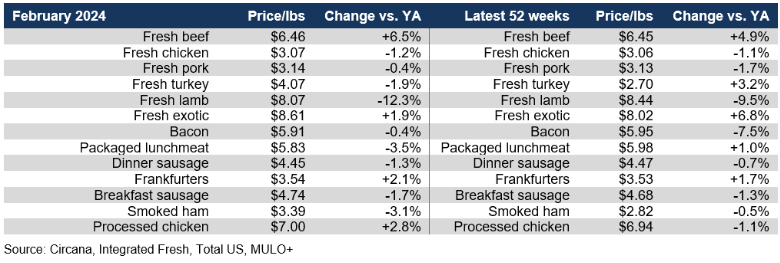

The average price per pound in the meat department across all cuts and kinds, both fixed and random weight, stood at $4.60 in February, up 1.% year-on-year. Processed meat tends to have the higher prices, but its average price per pound decreased for bacon, packaged lunchmeat, dinner and breakfast sausage, and processed chicken.

February brought year-on-year deflation for the vast majority of fresh and processed categories. Beef prices reflected a tight market once more.

Meat sales

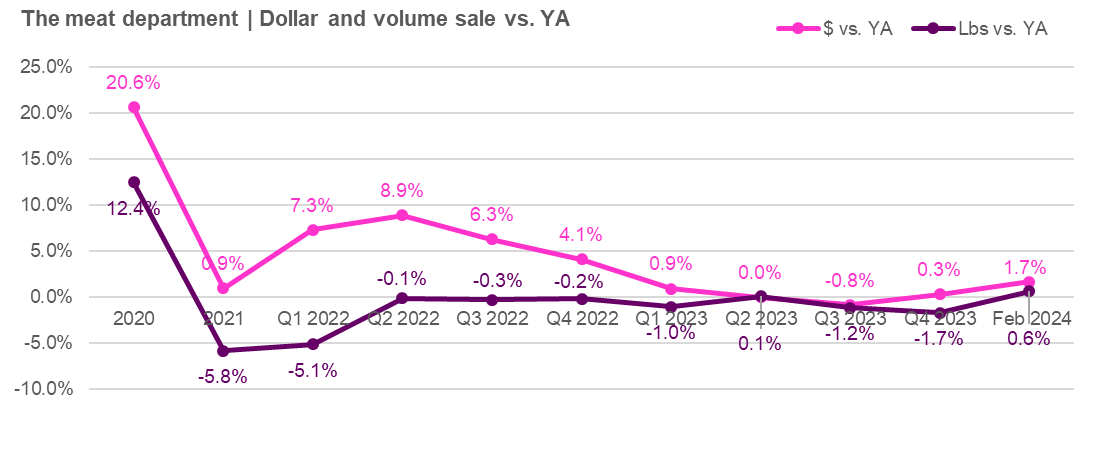

January brought a welcome change for the meat department with an increase in dollars and pounds. February continued to strong start of the year, especially in fresh meat. On an annual basis, pounds are getting closer to their prior-year levels as well.

The four February weeks have fairly consistent sales. Somewhat surprisingly, Valentine’s Day week did not show an elevated level of sales as seen in seafood. Year-on-year, it was also the only week with a decrease in pound sales in comparison to last year.

In the MULO+ universe, the meat department volume sales, both fixed and random weight, fell behind year-ago levels throughout 2023 – albeit not by much. As price increases started to moderate, the strong engagement with fresh meat has driven volume gains in both January and February of 2024 when compared to their year-ago levels.

Assortment

Meat department assortment, measured in the number of weekly items per store, averaged 428 SKUs in February 2024 — holding steady around 50 items below pre-pandemic levels.

Fresh meat sales by protein

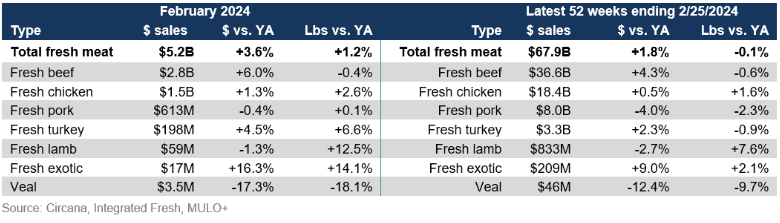

Fresh experienced a strong performance in February, with pound gains for chicken, pork, turkey, lamb and fresh exotic (which includes bison). In the full year view, dollars remained in the plus whereas pounds were about 0.1% behind prior year levels.

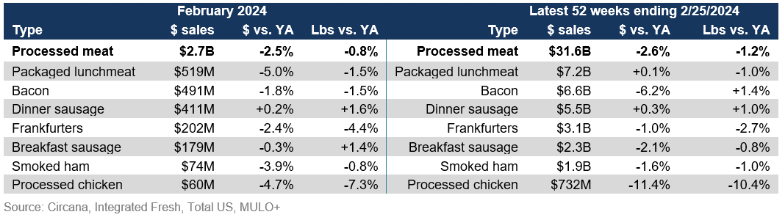

Processed meat

February processed meat sales were less than half that of fresh meat, at $2.7 billion. Dollar sales were down 2.5%, whereas pounds were mostly flat. Several subcategories did grow pound sales in February, including dinner and breakfast sausage.

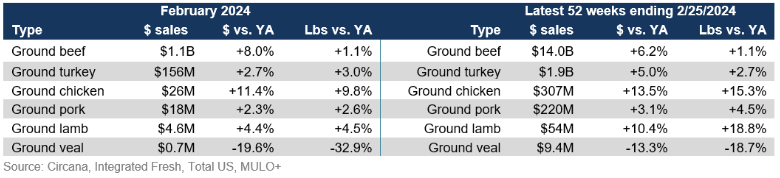

Grinds

The strong beef performance was driven by ground beef, which had a 1.1% increase in pounds. All smaller grinds, including turkey, pork and chicken, gained in both pounds and dollars in February as well.

What’s next?

According to the February Circana survey of primary grocery shoppers, Easter remains a big selling opportunity for grocery retail. However, the early timing of Easter Sunday on March 31st makes for the shortest selling season in several years – emphasizing the need for strong seasonal execution.

- One-third of shoppers do not plan any special celebrations, but 14% of those who do expect they will spend a little more on Easter groceries this year.

- The average Easter party size increased to an average of seven to eight people.

- Several retailers are offering meal bundles, predominantly aimed at dinner but some also including meal deals for Easter brunch. Many are combining meat department classics including ham and lamb with deli-prepared sides — leaning into convenience as consumers continue to skipper between time, cost, health, taste and nutrition.

The next performance report in the Circana, 210 Analytics and Hillphoenix series will be released mid-April 2024 to cover the March sales trends.

Date ranges:

2023: 52 weeks ending 12/31/2023

January 2024: 4 weeks ending 1/28/2024

February 2024: 4 weeks ending 2/25/2024

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!