The meat department starts off 2021 with accelerated gains

While early on in the pandemic many shoppers started out indulging in traditional and “comfort food” choices, January kicked off with New Year’s resolutions for 64% of shoppers. More than one third, 35%, aim to eat healthier, in general; 35% want to get more exercise; and 29% plan to save more money, according to the IRI Consumer Network survey conducted in January 2021. For meat, this means the consumer’s eye is on nutrition as well as price and promotion.

January saw a recovery of trip frequency to slightly above year ago levels while the basket size remained highly elevated. This resulted in high gains over January 2020 levels for total edibles, which is all food and beverage related items, at +12.7%. This is up significantly from a subdued December (+8.1%).

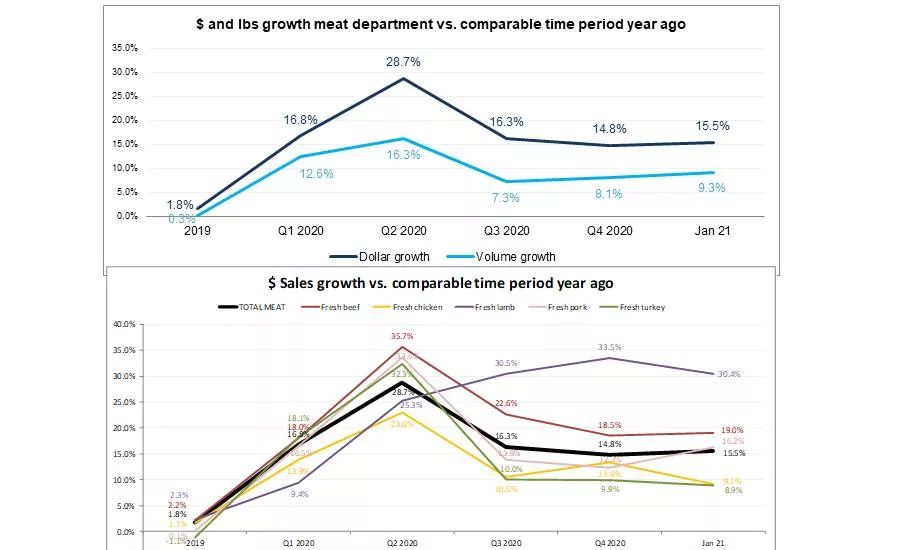

January meat department sales increased 15.5%, excluding online-only and delivery e-commerce sales, but does include pick-up-in-store fulfillment like click-and-collect and personal shopper delivery. IRI shopper research finds that 16% of shoppers are ordering their groceries online more, with all but 6% of opting for click-and-collect fulfillment versus direct-to-home delivery or pureplay online with no physical store. All in all, meat department multi-outlet sales for the four weeks ending January 24th gained an additional $823 million versus the comparable period in 2020.

The meat department dollar sales gain of 15.5% exceeded that of the fourth quarter and, importantly, the volume gains were the highest since the second quarter of 2020, at +9.3%. Dollars and volume trended 6.2 points apart — significantly closer than during most of 2020.

Fresh meat made up the majority share of sales, at $4.1B and had slightly higher gains (+15.6%) than processed meats (+15.3%) in January 2021. However, volume gains were slightly higher for processed meats, at +9.5%. That resulted in the gap between volume and dollars falling below the six percent mark for processed meats, whereas fresh remained at 6.4 percentage points.

Price per Volume

Most proteins saw significant increases in the price per volume throughout 2020. In January 2021, the price per volume for beef, chicken and lamb remained at least +5.0% over year ago levels, whereas the price of pork and turkey was more in line with January 2020. Prices across the meat department in January 2021 were up 5.7% over year ago. Note: Pork does not include Smoked Ham, which is reported in Processed Meats.

|

Average price per volume and change |

|||||||

|

|

2019 |

Q1 20 |

Q2 20 |

Q3 20 |

Q4 20 |

Jan 21 |

|

|

Meat department |

$3.53 |

$3.72 |

$3.99 |

$3.96 |

$3.51 |

$3.85 |

+5.7% |

|

Total fresh meat |

$3.35 |

$3.55 |

$3.92 |

$3.78 |

$3.30 |

$3.67 |

+5.8% |

|

Total processed meat |

$3.96 |

$4.13 |

$4.15 |

$4.39 |

$4.01 |

$4.27 |

+5.3% |

|

Fresh beef |

$4.88 |

$4.97 |

$5.82 |

$5.42 |

$5.21 |

$5.19 |

+5.3% |

|

Fresh chicken |

$2.33 |

$2.40 |

$2.45 |

$2.46 |

$2.43 |

$2.51 |

+5.0% |

|

Fresh pork |

$2.66 |

$2.78 |

$3.02 |

$2.81 |

$2.72 |

$2.77 |

+2.3% |

|

Fresh turkey |

$2.03 |

$3.14 |

$3.25 |

$3.43 |

$1.51 |

$3.05 |

+1.1% |

|

Fresh lamb |

$7.79 |

$7.91 |

$8.24 |

$8.51 |

$8.31 |

$8.22 |

+9.3% |

Source: IRI, Integrated Fresh, Total US, MULO, price per volume and % gain versus YA

Assortment

Assortment dropped by more than 65 items during some of the tightest supply weeks in May and June of 2020. In January 2021, assortment averaged 563 items per store, which was down about 3.6% versus year ago levels, although not all new item codes may be tallied just yet.

Fresh Meat Gains by Protein

In January 2021, beef accounted for 64% of all additional dollars over this month in 2020, reflecting a share gain of 19.0% over year ago. Chicken was the second-largest contributor to sales gains, at +$90 million versus year ago. Lamb had the highest percentage dollar gains, at +30.4%, but off a much smaller base.

|

January 2021 |

Dollar sales |

Dollar gains |

Absolute dollar gains |

Volume gains |

|

Meat department |

$6.1B |

+15.5% |

$823M |

+9.3% |

|

Total fresh meat |

$4.1B |

+15.6% |

$559M |

+9.2% |

|

Fresh beef |

$2.2B |

+19.0% |

$359M |

+13.1% |

|

Fresh chicken |

$1.1B |

+9.1% |

$90M |

+3.9% |

|

Fresh pork |

$549.6M |

+16.2% |

$77M |

+13.6% |

|

Fresh turkey |

$164.6M |

+8.9% |

$14M |

+7.7% |

|

Fresh lamb |

$39.2M |

+30.4% |

$9M |

+19.3% |

Source: IRI, Integrated Fresh, MULO, % growth versus year ago

Lamb has had the highest percentage gains since the third quarter of 2020 and has remained very stable at around 30-34% over year ago levels. Beef, while the largest of the fresh proteins in dollar sales, has consistently posted the second-highest growth, in the high teens. Chicken and turkey gains have been in the high single, low double digits in the last few quarters and January 2021. Turkey saw high levels of promotional discounts in the fourth quarter and low inflation in January.

Processed meats had a very strong start of the year as well. Bacon generated the highest sales, at $489 million, as well as the highest gains, at +22.9% in January 2021 versus year ago.

|

|

$ sales gains versus comparable period year ago |

||||||

|

|

2019 |

Q1 20 |

Q2 20 |

Q3 20 |

Q4 20 |

Jan 21 |

|

|

Meat department |

$3.53 |

$3.72 |

$3.99 |

$3.96 |

$3.51 |

$3.85 |

+5.7% |

|

Processed meat |

+1.9% |

+16.6% |

+22.5% |

+13.0% |

+12.8% |

+15.3% |

$2.0B |

|

Bacon |

+2.9% |

+13.9% |

+33.0% |

+17.8% |

+19.0% |

+22.9% |

$489M |

|

Packaged lunchmeat |

-0.6% |

+13.3% |

+11.4% |

+5.4% |

+9.8% |

+8.0% |

$412M |

|

Dinner sausage |

+2.6% |

+21.6% |

+32.2% |

+15.9% |

+13.8% |

+17.7% |

$338M |

|

Breakfast sausage |

+1.8% |

+14.3% |

+35.8% |

+20.0% |

+13.6% |

+19.2% |

$164M |

|

Frankfurters |

+0.2% |

+24.0% |

+22.5% |

+15.8% |

+17.1% |

+11.8% |

$170M |

|

Smoked ham |

-0.9% |

+32.7% |

30.7+% |

+17.1% |

+3.8% |

+11.7% |

$88M |

|

Processed chicken |

+1.4% |

+16.6% |

+14.0% |

+10.8% |

+16.3% |

+11.8% |

$48M |

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. YA

Grinds

In January 2021, the dominance of grinds in meat sales continued. Ground beef sales totaled $862.8 million or 217 million pounds. Ground beef alone added $69 million versus year ago levels in January. Altogether, the meat grinds listed below generated an additional $83 million during the four January weeks versus an additional $236,000 for refrigerated plant-based meat alternatives.

|

% sales change (January 2021) versus year ago |

Dollar sales |

Dollar gains |

|

Ground beef |

$862.8M |

+8.7% |

|

Ground chicken |

$18.7M |

+18.7% |

|

Ground lamb |

$3.5M |

+35.3% |

|

Ground plant-based meat alternatives |

$4.8M |

+5.1% |

|

Ground pork |

$14.8M |

+11.9% |

|

Ground turkey |

$122.9M |

+7.4% |

|

Ground veal |

$1.0M |

+15.3% |

Source: IRI, Integrated Fresh, Total US, MULO, % change vs. YA

What’s Next?

January showed that everyday demand continued to hold at double-digit above year ago levels. February has a strong sales opportunity in Valentine’s Day — traditionally a big out-of-home dining occasion, particularly in years where the holiday falls on the weekend. Additionally, continued high counts of COVID-19 cases and cold weather gripping much of the country should spell a more at-home focused occasion than in years past.

Looking further into the future, working from home full time is expected to remain more than twice as high as pre COVID-19: 44% of employed Americans expect to work from home at least once a week after the vaccine is widely distributed and restrictions are lifted, according to the January wave of IRI shopper research.

Likewise, the majority of children were still participating in remote learning in January. About six in 10 school-aged children were in a remote-only model and another 15% in a hybrid approach. Schooling patterns were similar for younger kids, ages 6 to 12 as they were for teens.

Nearly four in 10 (39%) shoppers expect the health crisis to last more than 12 more months, with an additional 32% expecting it to last another seven to 12 months.

Interest in getting the COVID-19 vaccine grew slightly over the past month:

- 7% have already received the vaccine (one or both doses), up from 3% in December

- 39% plan on getting it as soon as the vaccine is available to them, unchanged from December

- 14% plan to wait a few months or at least six months before taking the vaccine, unchanged from December

- 21% do not plan on taking it, down from 23% in December

- 21% are unsure, unchanged from December.

Source: 210 Analytics

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!